Weee! vs. Instacart

Jan-Erik Asplund

Jan-Erik Asplund

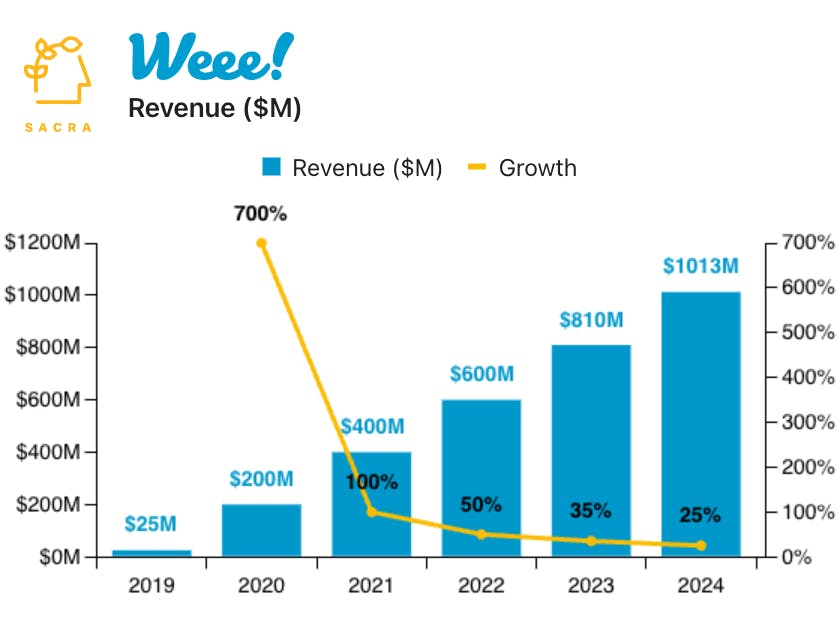

TL;DR: Starting as a WeChat group-buying service for Asian groceries, Weee! has evolved into a vertically-integrated online ethnic supermarket capturing 40-50% of customers' monthly grocery spend through specialized selection and 30-50% lower prices than local markets. Sacra estimates Weee! hit $1.013B in revenue in 2024, up 25% from $810M in 2023. For more, check out our full report and dataset on Weee!

Key points via Sacra AI:

- Initially launched in 2015 as a WeChat group-buying service connecting wholesale vendors with Chinese immigrants in the Bay Area—Weee! leveraged those connections to suppliers to launch a marketplace in 2017, directly sourcing fresh fruits, produce and other items from 300+ American producers and exclusive Asian partners and delivering through their own last-mile network of distribution hubs and delivery drivers. Unlike local Asian markets that rely on regional distributors/middlemen, Weee!’s direct sourcing enables higher gross margin (25-30% vs traditional grocers' 15-20%) and prices that are up to 50% lower, driving high average order value (~$250 monthly spend).

- As Weee! has grown from 9 states to delivering 40K daily orders across the entire contiguous United States, Sacra estimates Weee! generated $1B in revenue in 2024, up 25% from $810M in 2023, last valued at $4.1B in their $425M February 2022 Series E led by SoftBank Vision Fund for a 6.8x multiple on 2022 revenue of $600M. Compare to traditional Asian grocery chains like H-Mart with $2B in revenue from 100+ physical stores and 99 Ranch Market with 69 stores, while venture-backed ethnic e-grocery competitors like Umamicart, Sarap Now, and Kim'C Market maintain smaller regional footprints with 5-10% market share—and online grocery incumbent Instacart (NASDAQ: CART) at 800k daily orders and $3.3B in trailing twelve month revenue (15% take rate on delivery vs. Weee!’s full retail margin as a direct sell), growing 9% YoY, valued at $12.6B for a 3.8x multiple.

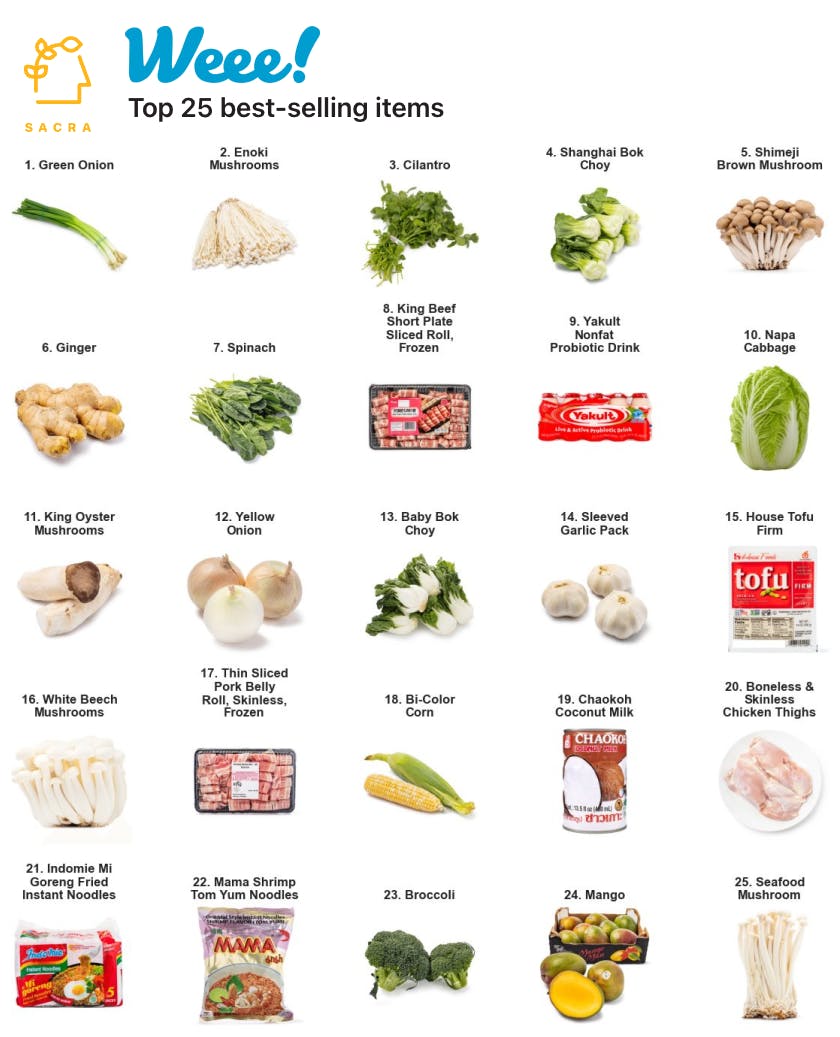

- With Americans increasingly consuming ethnic foods—e.g., Korean food consumption among non-Asians is up 127% since 2017—Weee!’s customer base has become 30% non-Asian American, setting the stage for Weee!’s transition from niche marketplace to the ethnic food aisle for the internet. At 10,000+ SKUs growing by 500 per week with expansion into Vietnamese (2% of their best-selling items sold), Indian (1%), and Thai (8%) cuisines, Weee!’s focus on 1) high-quality perishables (fruits and vegetables represent 57% of the 100 best-selling items) and 2) niche ethnic goods like Yakult milk drink and Lao Gan Ma chili crisp has it capturing 40-50% share of its customers' monthly grocery budgets (vs. 5-6% for Instacart), with $250 average monthly spend and 2.3x purchases per month.

For more, check out this other research from our platform:

- Weee! (dataset)

- GrubMarket (dataset)

- Swiggy (dataset)

- Instacart vs Amazon vs Uber

- Pradeep Elankumaran, CEO of Farmstead, on the future of online grocery

- Online Grocery Unit Economics, Sensitivity Analysis and TAM

- The Key Profitability Levers in Online Grocery

- Sebastian Mejia, co-founder of Rappi, on building for multi-verticality in on-demand

Read more from

Read more from

Read more from

Read more from

Fanatics vs. Kalshi

Free Report

Continue Reading

Dossier revenue, growth, and valuation

Unlocked Report

Continue Reading

Quince revenue, growth, and valuation

Unlocked Report

Continue Reading