+2 others

Booking.com of robotaxi

Jan-Erik Asplund

Jan-Erik Asplund

TL;DR: After $30B+ burned in the first AV wave, end-to-end neural networks have made autonomous driving viable again with vertically integrated operators (Waymo, Tesla) taking on aggregators (Uber with 25+ AV partnerships) & B2B software companies (Wayve, Applied Intuition) licensing driving brains to OEMs. For more, check out our full report and dataset on Waymo.

We previously covered AV leader Waymo (May 2026) and autonomy software provider Applied Intuition (July 2025, May 2026) as two of the biggest companies in the 2nd-generation of autonomous driving.

Key points via Sacra AI:

- After the first autonomous vehicle wave (2015-2022) burned $30B+ and ended in Cruise, Argo AI and Uber ATG shutting down, we saw 1) end-to-end neural networks replacing hand-coded rules and maps, and 2) AI-generated simulations replacing physical test miles at a fraction of the cost, enabling autonomous vehicle companies can now expand to new cities and geographies far faster than 1st-generation companies ever could. New-city expansion no longer requires months of mapping, local validation and custom engineering for every edge case, giving second-gen startups like Wayve ($2.8B raised, $8.6B valuation) and Waabi ($1.28B raised) a shot at building autonomy stacks with 3-5x less capital than first-wave Cruise ($10B+ spent), Waymo ($27B+ raised) and Aurora ($3.46B raised).

- Two companies emerged from the first wave with the balance sheets and data to lead: Waymo, backed by $27B+ in cumulative Alphabet funding and generating a Sacra-estimated $355M in annualized revenue as of February 2026 across ~500,000 weekly paid rides in 11 U.S. cities, and Tesla, which is building its robotaxi on top of a consumer self-driving fleet of 7M+ vehicles generating ~1 billion miles of driving data per month. Waymo grew 117% year-over-year from $131M in annualized revenue at the end of 2024 to $284M at the end of 2025, then hit $355M at the end of February 2026, valued at $126B as of their February Series D for a 355x forward revenue multiple, while Uber (NYSE:UBER) generated $52B in revenue in 2025, up 18% YoY, valued at $149B for a multiple of 2.9x.

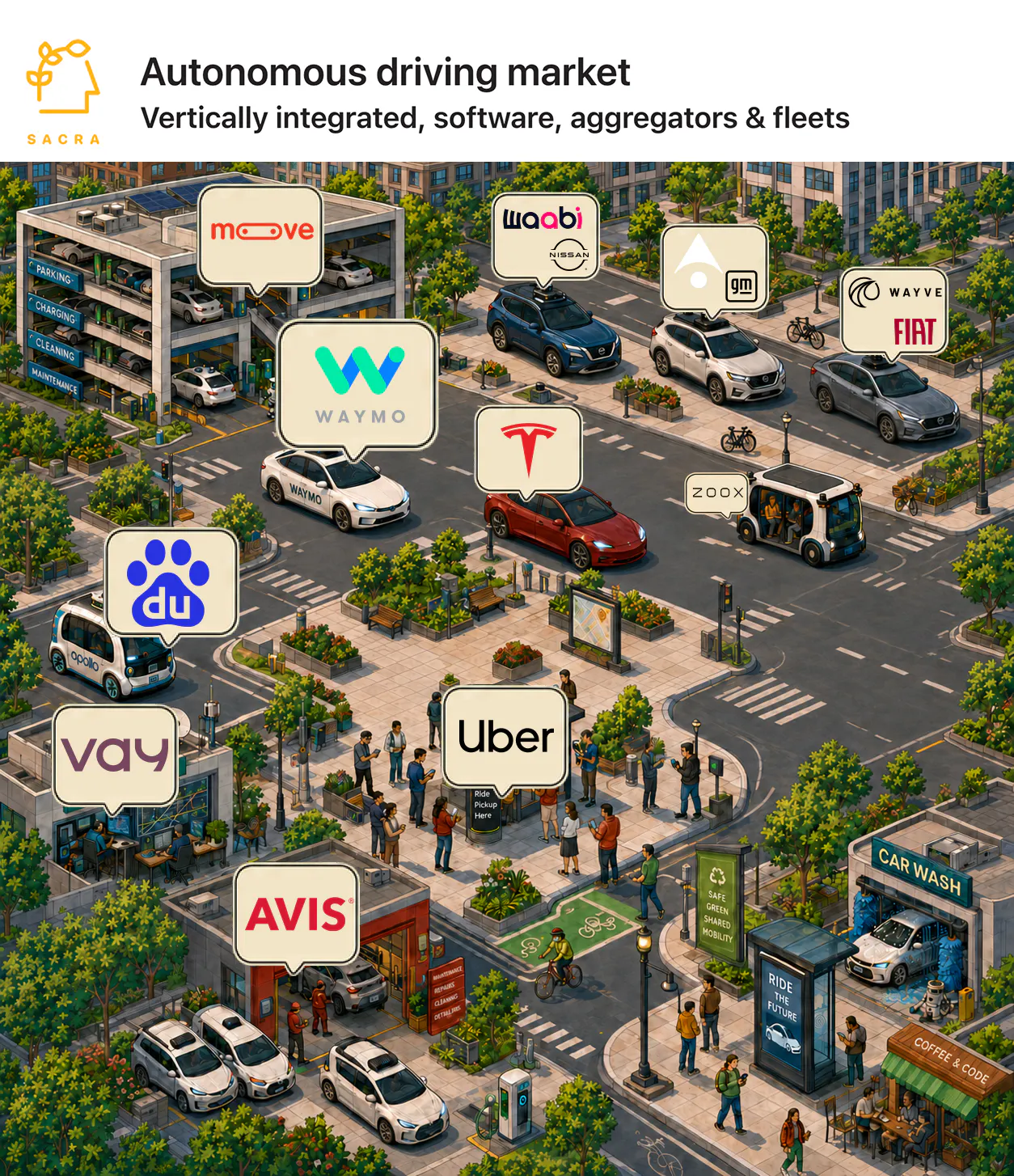

- The market is sorting into four layers: 1) vertically integrated robotaxi operators like Waymo, Tesla and Zoox that own the vehicle, the autonomy stack, the fleet and the customer relationship, 2) B2B software companies that license the AI driving brain to OEMs like Wayve, Applied Intuition, Mobileye and Nuro, 3) demand aggregators like Uber that route riders to whichever autonomous vehicle is nearest, and 4) fleet infrastructure providers like Moove ($400M ARR in June 2025, up from $275M in 2024), Vay and Avis that finance, maintain and operate the physical cars. Operators like Waymo capture the full fare at roughly 60% contribution margins but have to finance $50-175K vehicles and launch city-by-city, companies like Applied Intuition ($830M ARR, ~80% gross margins) get software economics but wait through 3-5 year OEM development cycles, while aggregators like Uber can hit ~60% gross margin with robotaxis rather than human drivers.

- After selling its own self-driving unit to Aurora in 2020, distribution king Uber (~300M weekly rides through its platform) has repositioned as the Booking.com of robotaxis, signing 25+ partnerships with Waymo (~500K weekly rides), Zoox, Wayve, Waabi, Nuro, WeRide and Baidu and taking a commission on every autonomous ride regardless of whose technology powers the vehicle. By signing every major AV operator onto its platform, Uber looks to commoditize the complement of autonomous driving as its uneasy Uber-plus-Waymo alliance takes on Tesla, which has a much smaller robotaxi fleet (~42 cars) in three Texas cities vs. Waymo’s (~4,000 cars) but charges ~$2/km vs. Waymo’s $5.70/km, betting that 1B+ monthly consumer miles and an owner revenue-sharing model where drivers opt their cars into the network can bypass the aggregator layer entirely.

- The most-funded pure-play software company in the space, Wayve ($2.8B raised, $8.6B valuation), is building a hardware-agnostic end-to-end AI driving model, selling to Uber which wants long-term optionality to power robotaxis on any vehicle platform, and to OEMs like Nissan & Stellantis who want to add autonomy without it being a core competency. Wayve has driven in 500+ cities across Europe, North America and Japan without mapping any of them, but without their own cars, the upside depends on OEM development cycles that run 3-5 years converting to production contracts, while Stellantis is hedging by investing in both Wayve and Applied Intuition ($830M ARR, $15B valuation, ~80% gross margins, 18 of the top 20 OEMs as customers) simultaneously.

- While Uber is profitable with a demand-aggregation model that can plug in any autonomous vehicle, Waymo has the most advanced full-stack robotaxi operation but burns ~$5B+ a year, a gap that explains their frenemy partnership dynamics where Waymo trades a cut of every Uber-routed fare for the demand density it needs while it races to drive vehicle costs down from ~$175K per Jaguar I-PACE toward a target of sub-$50K with a prospective Hyundai deal while pushing utilization from 35% toward 55%+. At current scale, each of Waymo's ~4,000 vehicles generates roughly $130K in annual gross revenue at 35% utilization, which barely covers the $175K cost of a Jaguar I-PACE but becomes a ~2.5x annual return on capital at sub-$50K vehicle cost and 55% utilization.

- While states like New York & Illinois block autonomous vehicles outright as part of the culture war, Chinese AV companies Baidu Apollo Go, Pony.ai, WeRide and Momenta are scaling with purpose-built robotaxis at 2-3x lower hardware costs, cheap domestic LiDAR and regulatory environments that let them move faster—posing the kind of exogenous competitive pressure that may do more to accelerate U.S. deployment than any domestic market force. With Baidu's RT6 costing $28-30K versus Waymo's sub-$50K target and robotaxi fares up 395% YoY in Q1 2026, the global market increasingly split between U.S. companies launching city-by-city at home and Chinese operators expanding through Uber, Lyft, Bolt and local partners across the rest of the world.

For more, check out this other research from our platform:

- Waymo (dataset)

- Waymo vs. Tesla vs. Baidu

- Moove (dataset)

- Applied Intuition at $830M/year up 2x YoY

- Applied Intuition at $415M/year

- Bobby Healy, CEO & founder of Manna, on drone delivery for the suburbs

- Orest Pilskalns, CEO of Skyfish, on building autonomous drone infrastructure

- Scale at $760M ARR

- Scale: the $290M/year Mechanical Turk of machine learning

- America First vs. American Dynamism

Read more from

Read more from

Waymo revenue, growth, and valuation

Unlocked Report

Continue Reading

Read more from

Arena revenue, growth, and valuation

Unlocked Report

Continue Reading

$100M/year Nielsen of LLMs

Free Report

Continue Reading

$20M/year Replit for GCs

Free Report

Continue Reading

Read more from

Moove revenue, growth, and valuation

Unlocked Report

Continue Reading