Revolut at $4B/year growing 75% YoY

Jan-Erik Asplund

Jan-Erik Asplund

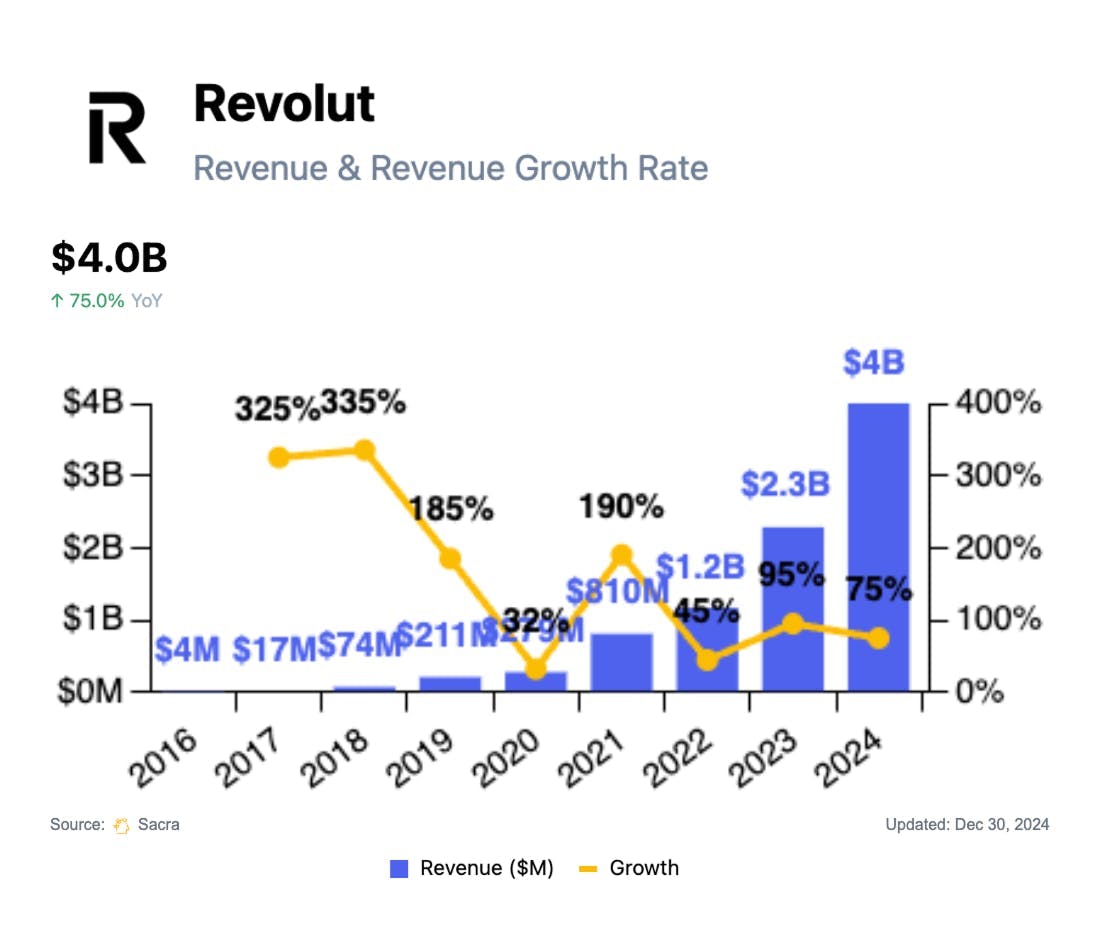

TL;DR: With the rise of mobile-first banking and crypto trading across Europe, Revolut has evolved from a zero-fee travel card into a financial super-app spanning payments, investing, and lending. Sacra estimates Revolut hit $4.0B in revenue in 2024, up 75% YoY from $2.3B in 2023, with its Wealth unit (crypto and stocks) growing 298% YoY to $647M. For more, check out our full report and dataset on Revolut.

Key points via Sacra AI:

- Founded in 2015 as a travel-focused FX card that undercut banks' 3-5% foreign exchange spreads with zero-fee interbank rates, Revolut expanded beyond its "must-pack travel accessory" positioning into P2P payments (2015), cryptocurrency trading (2017), stock trading (2019), and now UK banking (licence granted July 2024)—transforming from a single-purpose prepaid card into Europe's largest neobank. Revolut’s super app monetizes users across 1) spending (0.2–1.5% interchange, 0.8–1.2% merchant acquiring), 2) saving (~150bps net interest on £30B+ in deposits), 3) trading (0–0.09% crypto spreads, 0.25% stock fees), and 4) borrowing (~18% APR on credit), while layering on paid plans (£2.99–£55/mo) for FX allowances, perks, and loyalty.

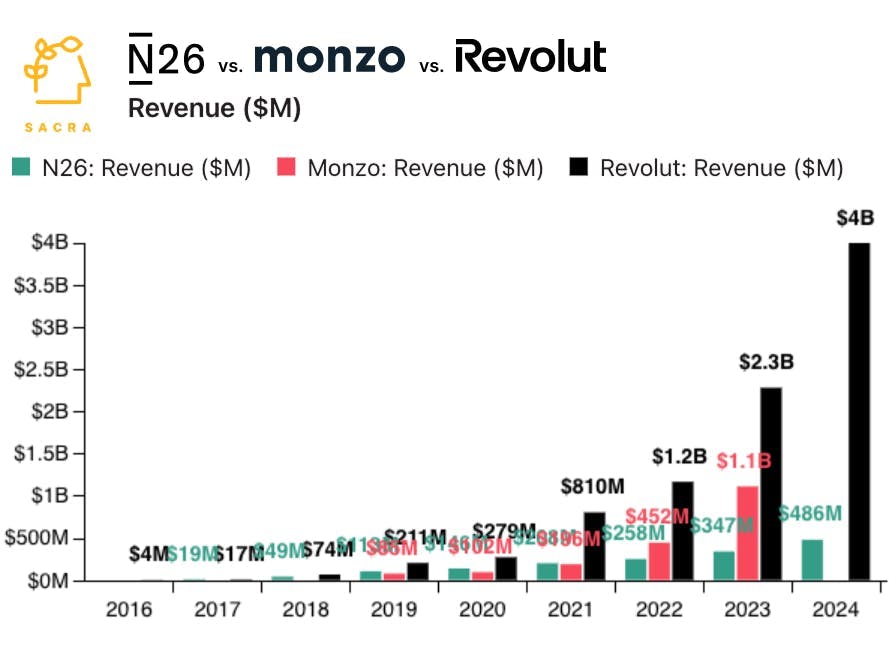

- Capitalizing on the crypto bull market where Bitcoin tripled and retail trading volumes surged across Europe, Sacra estimates that Revolut hit $4.0B in revenue in 2024, up 75% YoY from $2.3B in 2023, with Revolut Wealth (crypto and stock investing) as the fastest growing unit of business at $647M of revenue, up 298% YoY, valued at $45B for a 11.25x revenue multiple. Compare to European neobank peers Monzo at $1.1B revenue in 2023 (up 147% YoY) valued at $5.9B for a 5.4x multiple and N26 at $486M revenue in 2024 (up 40% YoY) valued at $6B as of 2023 for a 17.3x multiple on $347M in revenue, or to hybrid crypto-consumer American fintech Robinhood (NASDAQ: HOOD) at $2.95B revenue in 2024 (up 11% YoY) with a market cap of $57.5B for a 19.5x multiple.

- Following the success of Cash App’s addition of Bitcoin buy & sell (launched in 2018, $4.5B in Bitcoin sales in 2020)—along with early launches from Revolut (2017) and Robinhood (2018)—consumer fintechs across the board, from payments (PayPal) to brokerage apps (eToro) to neobanks (N26 & Nubank) have added crypto offerings and hybridized into fiat-crypto companies to deepen share of wallet. In building a consumer finance super app, Revolut is betting on its product velocity to bring together fiat & crypto and payments, neobank & brokerage with infrastructure laid out in the form of FX rails and Visa cards for spend, a Cyprus-based crypto entity for trading 150+ assets, and—soon—a UK banking licence for insured deposits and high-yield accounts.

For more, check out this other research from our platform:

- Revolut (dataset)

- Monzo (dataset)

- N26 (dataset)

- Chime (dataset)

- eToro (datase

- Ex-Chime employee on Chime's multi-product future

- The neobank capital cycle

- Arjun Sethi, co-CEO of Kraken, on building the Nasdaq of crypto

- David Ripley, COO of Kraken, on the future of cryptocurrency exchanges

- Wealthfront, Betterment, and the robo-advisor resurrection

- Founder of neobank company on the importance of picking the right sponsor bank

- Fintech investor on how banking-as-a-service platforms build partnerships

- Senior BaaS platform executive on the rise of banking-as-a-service 2.0

- Founder of startup card issuing platform on the competitive dynamics of card issuing

- Business development executive at a BaaS platform on differentiation and competitive dynamics in BaaS

- The future of interchange

- The neobank capital cycle

Read more from

Revolut revenue, users, growth, and valuation

Unlocked Report

Continue Reading

Read more from

Post-Brex Ramp vs Mercury

Free Report

Continue Reading

$200M/year Whop of B2B neobanks

Free Report

Continue Reading

Slash revenue, growth, and valuation

Unlocked Report

Continue Reading

Read more from

Read more from

Circle revenue, growth, and valuation

Unlocked Report

Continue Reading