Sentry: the $128M ARR error tracker disrupting New Relic

Jan-Erik Asplund

Jan-Erik Asplund

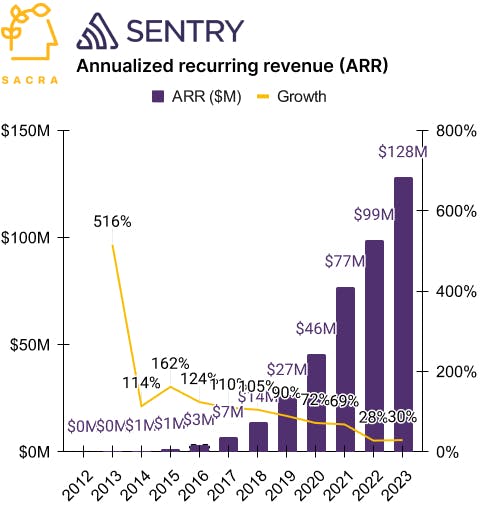

TL;DR: Sacra estimates that Sentry hit $128M annual recurring revenue (ARR) in 2023, growing 30% year-over-year, with 50,000 paying customers. Since becoming the biggest dedicated error tracking tool by revenue, they’ve shifted focus to competing with Datadog (NASDAQ: DDOG) and New Relic to own application performance monitoring (APM). For more, check out our report and full dataset on Sentry.

Key points from our research:

- Sentry (launched 2012) found product-market fit with its their software development kit (SDK) that lives inside your web or mobile app code and automatically captures errors, grouping and de-duplicating them and then sending them to a web UI with stack traces and device info for triage and debugging. First developed in 2008 as an open source project by Sentry co-founder & CTO David Cramer to help the Django web framework community with error tracking, it launched its cloud-hosted SaaS in 2012—by 2014, it was in use at Uber and Instagram, with high retention expansion from living inside the product with usage-based pricing, setting the stage for its product-led growth (PLG) motion ala Atlassian.

- Sacra estimates that Sentry hit $128M annual recurring revenue (ARR) on 50,000 customers by the end of 2023, growing 30% year-over-year, valued at ~23x its Series E financing at “over $3 billion” announced in May 2022. As it has grown, Sentry has prioritized self-serve (70% of total revenue) and kept sales & marketing headcount low ($366K ARR per head), investing in product & engineering to launch new products & features into their existing SDK to drive usage and expand into adjacent use cases, not unlike Docker ($135M ARR, ~$1687 average revenue per org).

- With the launch of performance monitoring, session replays, and code coverage, Sentry is now positioning as a bottom-up, developer-centric competitor to enterprise-focused incumbents like New Relic ($970M ARR) with their $58K ACV and Datadog (NASDAQ: DDOG, $2.4B ARR) at $78K. Sentry’s upside hinges on expanding the TAM for their self-serve offering from the $1B error tracking market to the $51B market (growing 11% yearly) for app performance metrics (APM), log management, and infrastructure monitoring.

For more, check out this other research from our platform:

- Sentry (dataset)

- Cribl (dataset)

- Retool: the $82M ARR internal app builder

- Retool (dataset)

- Blake Bartlett, partner at OpenView, on the future of product-led growth

- Docker (dataset)

- Snyk (dataset)

- Scott Johnston, CEO of Docker, on growing from $11M to $135M ARR in 2 years

Read more from

Sentry revenue, users, growth, and valuation

Unlocked Report

Continue Reading

Read more from

Mirakl at $218M ARR

Free Report

Continue Reading

Peec vs. Profound

Free Report

Continue Reading

Peec revenue, growth, and valuation

Unlocked Report

Continue Reading

Read more from

CodeRabbit vs. GitHub

Free Report

Continue Reading