Contractor Payroll: The $1.4T Market to Build the Cash App for the Global Labor Market

Jan-Erik Asplund

Jan-Erik Asplund

Deel launched out of Y Combinator’s Winter ‘19 batch as a way for companies to hire anywhere in the world.

Deel abstracted away the messiness of remote hiring, putting payments and compliance behind a simple SaaS interface.

Few launches have been as well-timed: in less than a year, worldwide COVID lockdowns hit and Deel took off, growing revenue 20x from $200K to $4M in 2020, and 13.5x from $4M to $54M in 2021.

But while Deel’s success heightened the attention on remote work and global hiring, the nature of Deel’s product-market fit has more to do with enabling teams to hire contractors than hire employees.

Join our list for more exclusive coverage and research on the private markets.

Success!

Something went wrong...

Today, freelancer earnings represent $1.4T of $25T in annual B2B payments. Of about 59 million people who work outside traditional employment structures, 85% or 50 million work as freelancers or contracted-out workers, per data from Wingspan, while only 15% are virtual laborers hired through platforms like Upwork, Uber, or Handy.

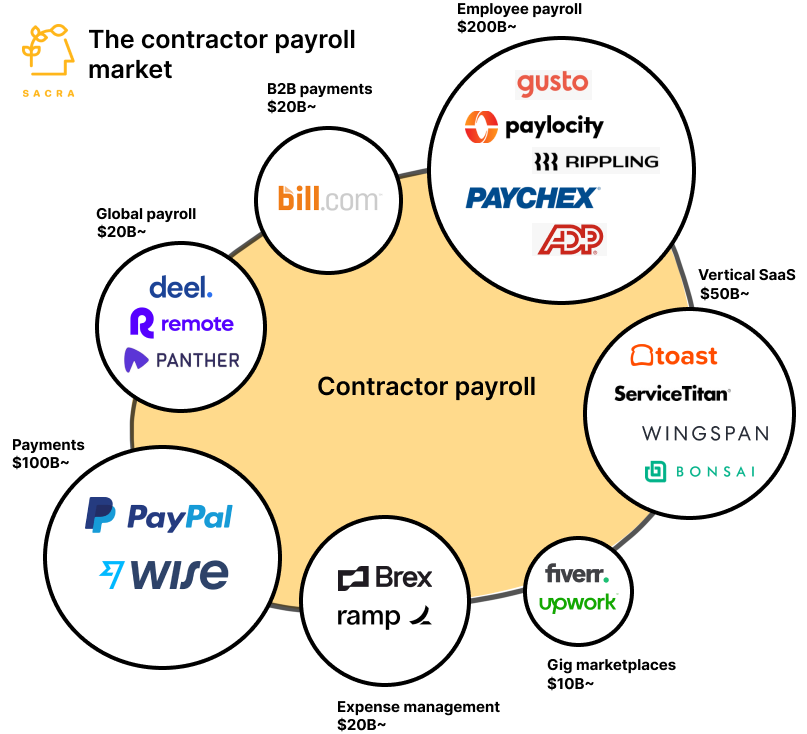

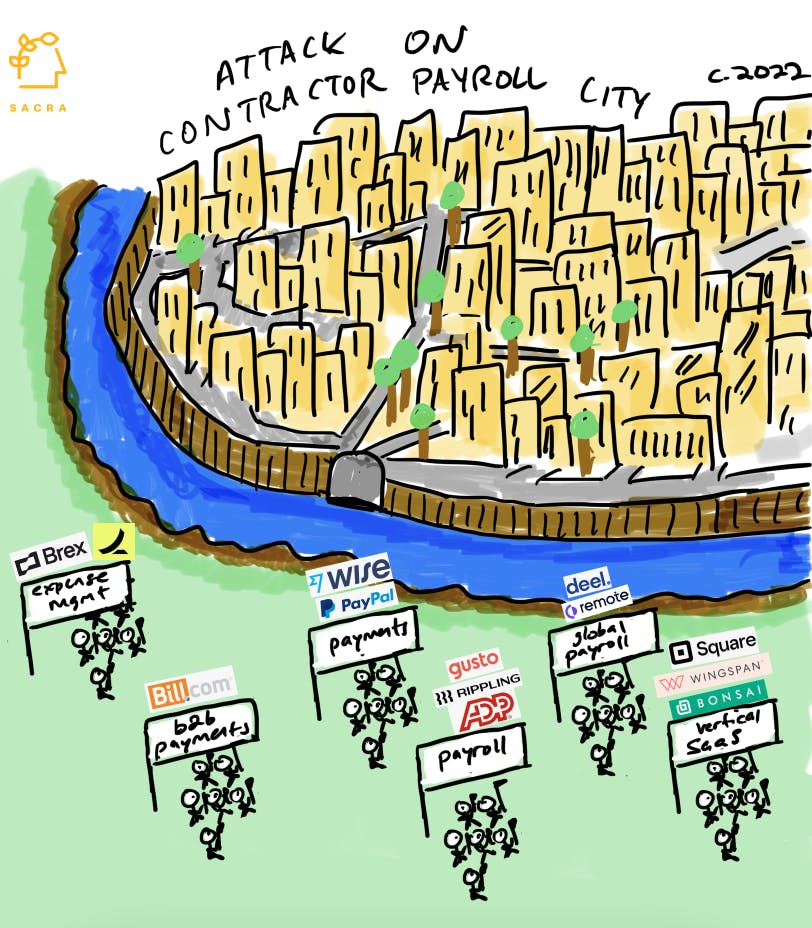

And Deel isn't the only company going after what we call “contractor payroll”—the combination of payments and SaaS built to help companies hire, onboard, work with and pay contractors at scale within a payroll-like OS.

Contractor payroll, on the contrary, is a space that is being contested by some of the biggest companies in B2B SaaS:

- Employee payroll companies like ADP, Rippling and Gusto are now launching features for paying contractors

- Vertical SaaS like Wingspan, Bonsai, and Contra are building tools and financial services specifically for contractors

- Gig marketplaces like Upwork, Fiverr, and Toptal connect companies and contractors and offer native payments

- Global payroll companies like Deel, Panther, Remote, and Papaya Global help companies build teams of international contractors

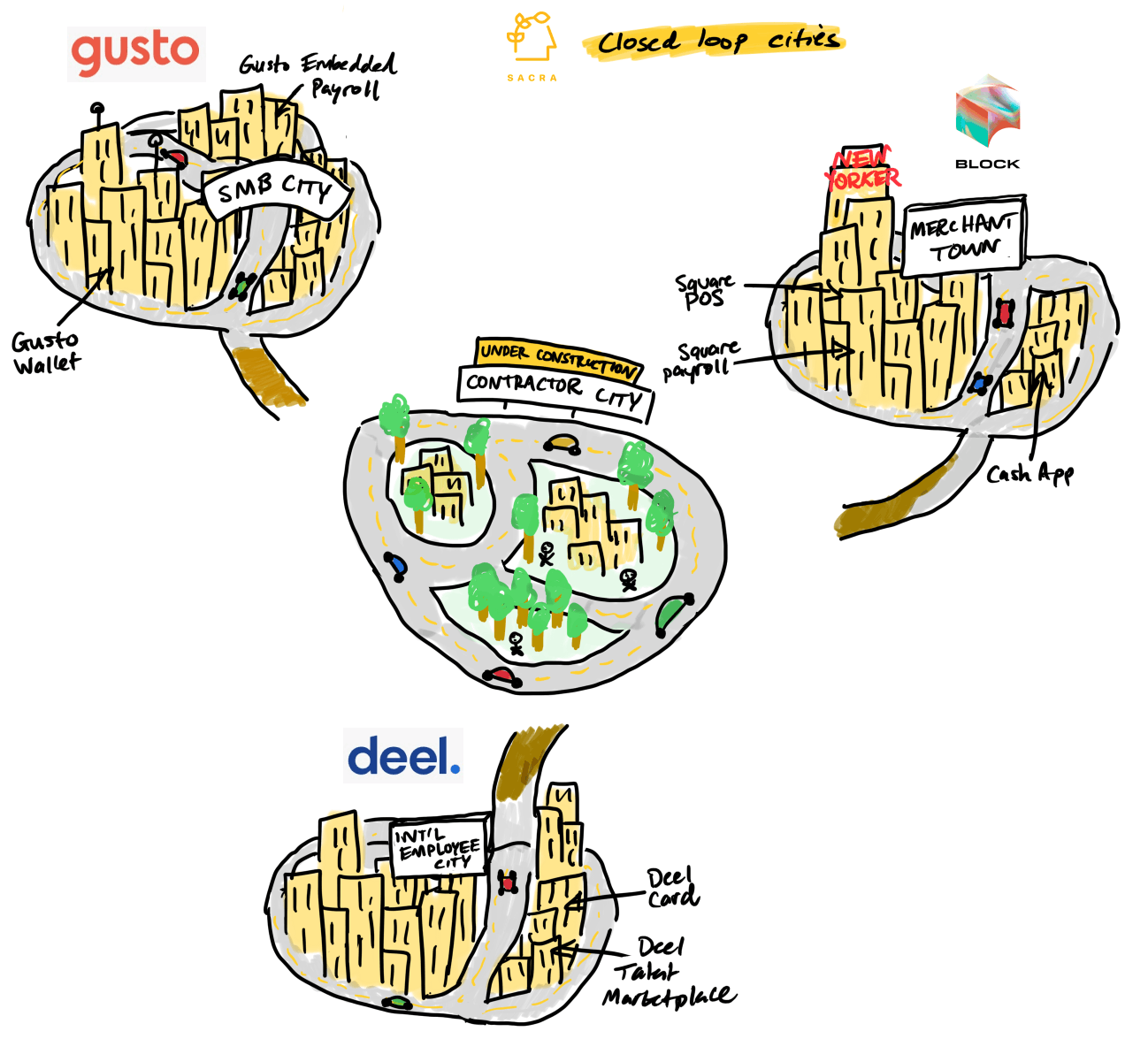

Each is looking to win contractor payroll because of the unique opportunity that it represents—to own the contractor wallet and build a closed loop payments network for the global labor market.

Key points

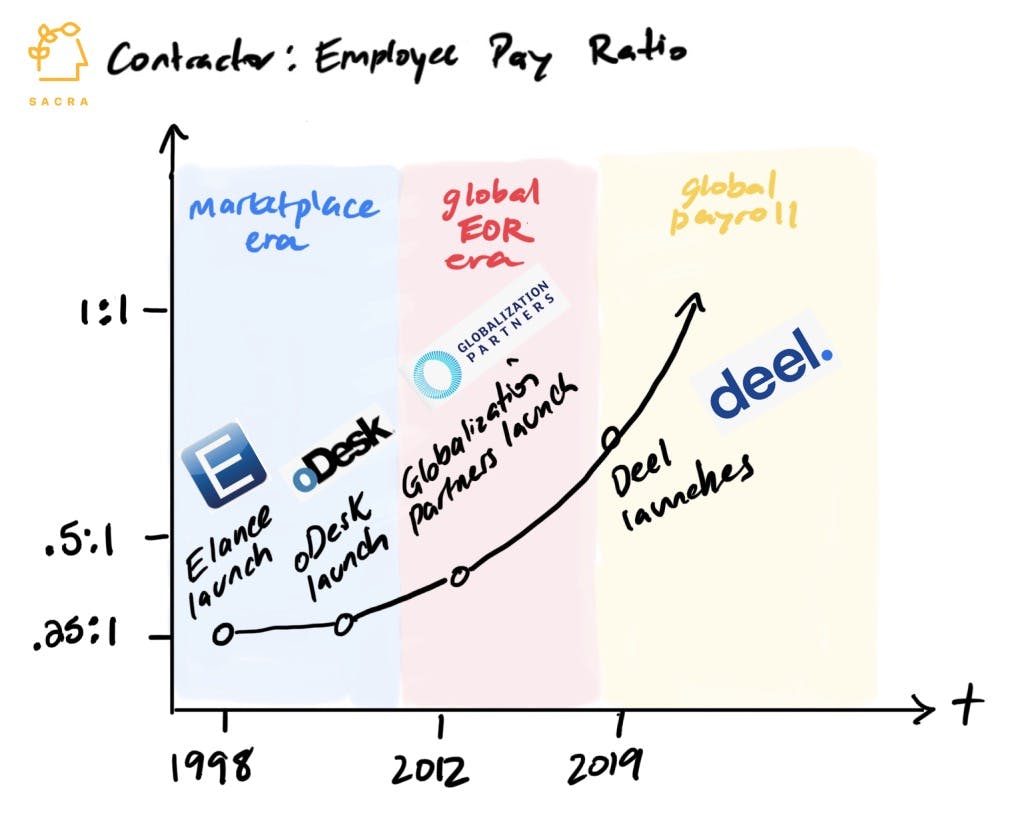

- In the first phase in the history of labor geo-arbitrage, gig work marketplaces like Elance/oDesk—now Upwork ($1.72B)—democratized geo-arbitrage for simple gig-like tasks. With these marketplaces, anyone could do offshore basic gigs—writing blog posts, designing illustrations, etc.—to countries with lower costs of living.

- Next, we saw employer of record companies like Globalization Partners ($4.2B) and Velocity Global ($500M raised) emerge to help companies offshore entire departments. Coming out of the Great Financial Crisis, these companies helped businesses geo-arbitrage at a greater scale.

- Today, we’re seeing global payroll companies like Deel ($12B), Remote ($3B) and Oyster ($1B) grow rapidly by helping companies geo-arbitrage from day 1, when building out their core team. With the rise of global talent, the rising cost of healthcare and benefits, and COVID as tailwinds, we've seen more and more companies looking to hire globally from the beginning.

- Deel’s initial product-market fit came from layering a payroll experience on top of international contractor payments—which we call “contractor payroll”—which abstracted away local compliance and enabled employers to pay their teams in local currency with a single click. Instead of paying for an EOR, you can hire your core team as contractors first—without relying on apps like Wise ($8B) or PayPal ($97B) that are built for one-off payments, require laborious record keeping and create legal/regulatory risk.

- Contractor payroll businesses combine the sticky, 90% retention business of payroll with an 80% gross margin SaaS workflow on top. Contractor payroll businesses drive SaaS revenue from access to their management/compliance features, and transactional revenue from the financial services they offer contractors/float/foreign exchange/interchange.

- Contractor payroll as a feature is becoming a part of many B2B products—from ADP ($96B) to Rippling ($11B), Bill.com ($12B) and Ramp ($8.1B)—as they compete to eat up all B2B transactions. Many of these companies are attacking the strategic chokepoint that is contractor payroll by weaponizing distribution and bundle economics they can use to win their target segment—from big companies hiring thousands of contractors like Wingspan ($20K-$70K ACV) to payroll providers like Gusto targeting SMBs.

- APIs like Check ($119M raised) and Zeal ($15.4M raised) and products like Gusto Embedded Payroll are trying to commodify contractor payroll by abstracting it into a set of APIs any vertical SaaS like ServiceTitan ($9.5B) or Toast ($9B) can use to pay contractors and employees. With embedded contractor payroll, vertical SaaS products can build stickier products and drive additional revenue.

- These companies want to own contractor payroll because contractors and companies are densely networked via payments graphs while employees are networked merely via professional graphs like LinkedIn. Owning that payments graph gives these companies access to a 60M+ user base with high stickiness, $1.4T in fund flows every year and growing, and a long list of monetizable products and services that can be sold into it.

- Competition creates fragmentation across the contractor payments network—where a company may prefer paying with e.g. Bill.com while the contractor prefers payment over PayPal—perpetuating the slowness/friction in contractor payments. The contractor payroll platform that wins will need a value proposition that brings both sides—companies and their freelancers—together on the same platform.

- The big opportunity to own contractor payroll is to build a closed loop network for the $1.4T and growing of freelancer payments made every year. Instead of just monetizing on the payer (company), these platforms are monetizing the payee (contractor) as well, and instead of being payroll-centric, payroll for these platforms is just a form of leverage to deploy a range of financial services.

- Where Gusto ($10B) changed payroll by eliminating physical pay stubs and bringing employers and employees onto shared web portals, contractor payroll companies are building vertically integrated portals that capture the network of companies and freelancers. On top of the core payroll solution, these platforms layer on other neobank-like products and services that help contractors and that can be monetized via fees and interchange.

- Cash App ($2B in gross profit/year) captured 70M consumer wallets by helping users get their money faster—today, contractor platforms can capture freelancer wallets by leveraging their position as payroll providers to do the same for contractors, who are paid late 30% of the time. By owning the contractor wallet with that 10x better experience, contractor payroll platforms then have an opening into selling a range of other products and services into their network.

- On top of that closed loop payments network, contractor payroll platforms have the opportunity to multiply ARPU 5-7x ala Cash App by layering on new products for 60M+ freelancers. The ultimate vision for contractor payroll platforms is to look more like a vertical SaaS family of products for the millions of freelancers around the world, including benefits, insurance, lending, recruiting, and more.

Business model: Payroll in the front, fintech in the back

Contractor payroll platforms turn the purely transactional business of contractor payments into subscription SaaS by layering a set of workflow products on top.

The core payroll business model is characterized by:

- Gross margin around 80%, with major costs composed of cloud hosting, executing payments (ACH, push to debit), and international banking and currency exchange

- Client retention around 90%, due to the high switching costs of swapping out your payroll provider

- Capital spend to total sales as low as 5% due to relative lack of fixed assets

Contractor payroll platforms charge customers a monthly fee to access their payments and compliance tools. They will also charge an additional per-seat fee based on the number of contractors that a company is paying.

Most revenue, however, comes from how they monetize their customers’ total payroll volume via:

- Markups on financial services: Contractor payroll companies make money by selling financial services into the contractors that use their product, like instant transfers of wages to bank accounts.

- Interest on float: Many financial services and payments products make money by lending out float—money held by a platform that’s in the process of clearing an account

- Foreign currency exchange: By charging the contractors a small fee for currency conversion on international transfers, the platforms get another source of revenue while making the exchange feel “free” for the company.

- Interchange split: Contractor payroll platforms make about $1.05 per every $100 that a contractor spends using their virtual card via interchange: the fee set by card networks for using their payment rails to move money

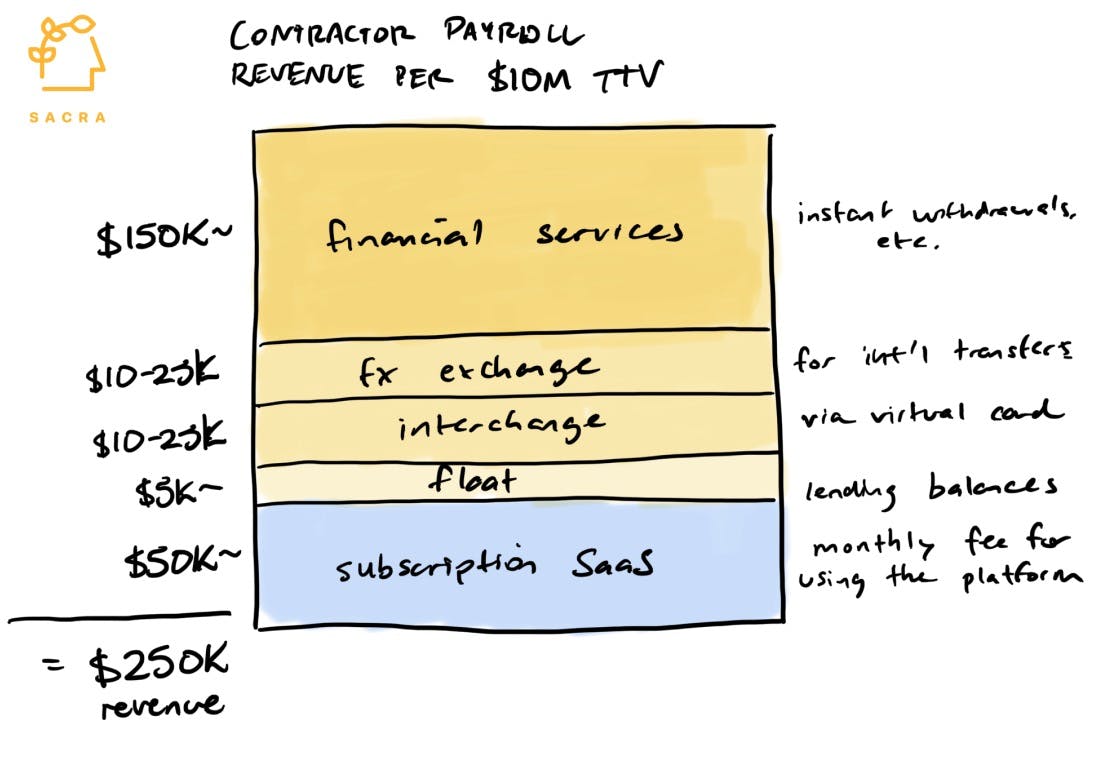

The upshot is that a company paying out $10M a year to 600 independent contractors can generate about:

- $50K per year in SaaS revenue assuming a $5 per-seat fee.

- $250K in transactional revenue at an average monetization rate of 2.5%.

Financial services are likely to be the biggest driver of transactional revenue for mature contractor payroll companies: if half of the contractors at a company doing $10M in payment volume per year opt into instant payouts, and the platform charges a 1% markup, that’s $50K in revenue.

Float revenue is likely to decrease over time. For example: Bill.com ($12B) started monetizing off float after introducing bill payments in 2009. As late as Q3’19, float was 22% of revenue. As of Q3’22, with the rise of features like Instant Transfer, it’s down to 1%.

Contractor payroll platforms also make some money via the international currency exchange necessary every time a company wants to pay a contractor in a different country.

Analysis: The twilight of labor geo-arbitrage

In the 90’s, the grandaddy of geo-arbitrage, GE CEO Jack Welch, moved all of GE’s IT services to India to save money.

Other big American companies would go on to do the same, like IBM, whose Indian workforce grew from 3,000 in 2002 to 53,000 in 2007.

Over the course of the 2000s, all American multinationals hired 2.4M foreign workers across countries like Mexico, India, China and Ireland while also reducing their total workforce by 2.9M—a total 5M+ total net increase in offshore employees.

The launch of platforms like Elance in 1998 and oDesk in 2003 promised to enable any company to offshore, as the marketplace era of labor geo-arbitrage kicked off.

Suddenly, anyone could go online and hire someone in a country with a lower cost of living for gigs like data entry, designing a website, or writing a blog post for significantly lower wages than a domestic employee would demand.

At IPO, Upwork (NYSE: UPWK)—the company formed when Elance and oDesk merged—reported having 2M+ unique projects on the platform, more than 375K freelancers earning an income, and 475K paying clients.

The era of the global EOR followed.

The rise of global EORs was fueled in part by the late 2000’s financial crisis. In its aftermath, companies began looking for ways to geo-arbitrage labor at a greater scale than just gig work and blog posts—they wanted, Welch-like, to build whole teams and departments out-of-country.

Companies like Globalization Partners (2012), Velocity Global (2013) and Papaya Global (2016) were founded to capitalize on this desire, providing companies with the material presence necessary for them to hire teams internationally.

Today, what we’re seeing emerge with companies like Deel (2019) is a new kind of relationship between companies and contractors.

Rather than bringing on international teams as a supplement to their existing domestic base, companies are building global teams using contractors from day 1.

They're hiring their core team as contractors, then only going through the significant costs of setting up a material presence in another country or using an EOR to scale.

Those contractors aren’t ancillary members of the team, or used only for tightly delimited projects—they behave more like employees, only employees that can be freely and cheaply hired from anywhere in the world to work anywhere in the world, with minimal bureaucracy, without needing to pay expensive healthcare and benefits upfront.

To enable this, the core thing that was needed was to eliminate the manual, repetitive, and time-consuming process of paying those contractors—to build a payroll-like experience so teams could pay their contractors as easily as they pay their regular employees.

1. How companies like Deel ($12B), Remote ($3B) and Oyster ($1B) grew fast by payrollifying the geo-arbitrage of labor

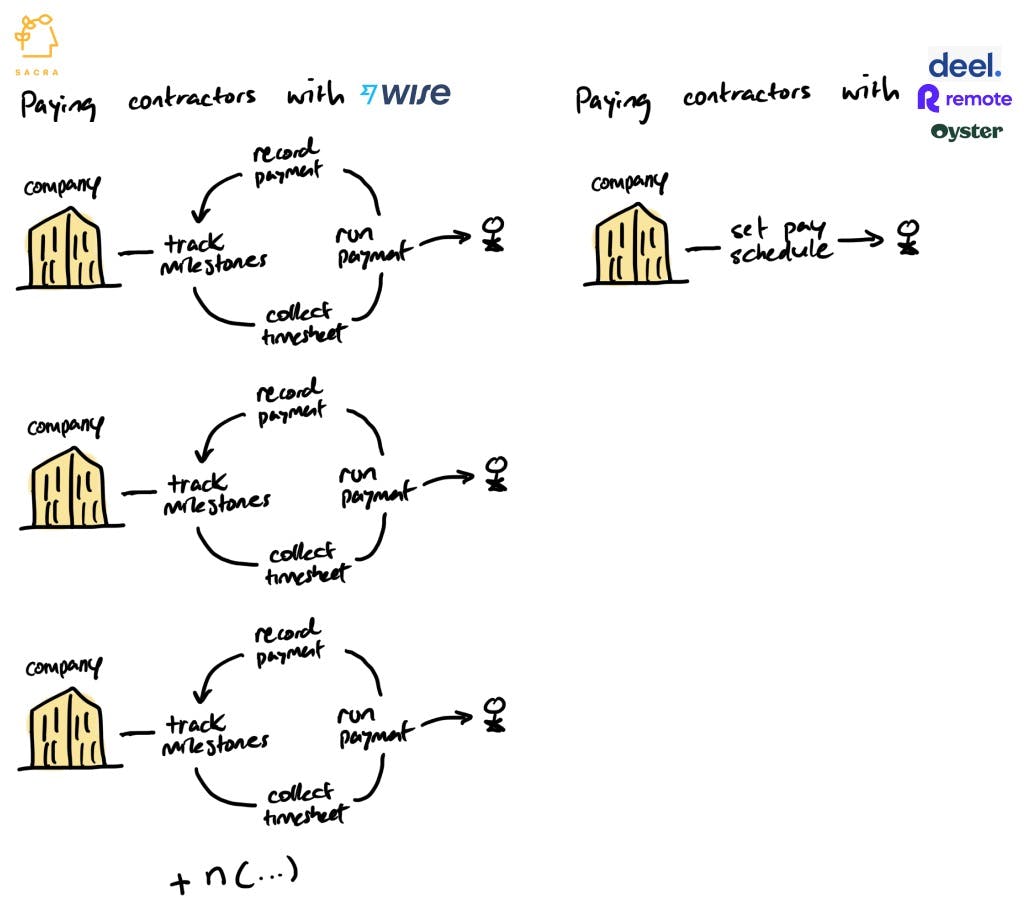

Before companies like Deel payrollified labor geo-arbitrage, startups would routinely pay contractors using P2P payments apps like Wise ($8B) and PayPal ($97B), B2B payments apps like Bill.com ($12B) or writing money directly out of their bank account.

- They’d need to pay legal fees to make sure they were staying compliant with each jurisdiction where they had workers, and they’d have to do the legwork themselves on figuring out how to offer insurance or any other benefits.

- They’d have to collect tax documentation from all those workers upfront, file at the end of the year, and keep track of all the payments they made—likely in an Excel spreadsheet.

As your number of contractors grew, this manual, one-off payments process and all the background moving parts would become a bigger pain.

What companies like Deel and Wingspan did was create a solution to help companies manage teams of contractors at scale by bundling payment tools like Wise into SaaS solutions for paperwork, invoicing, and compliance that give both company and contractor a payroll-like experience.

When COVID hit, these kinds of services enjoyed huge growth as the idea of building a global, remote team became, for many companies, the default choice:

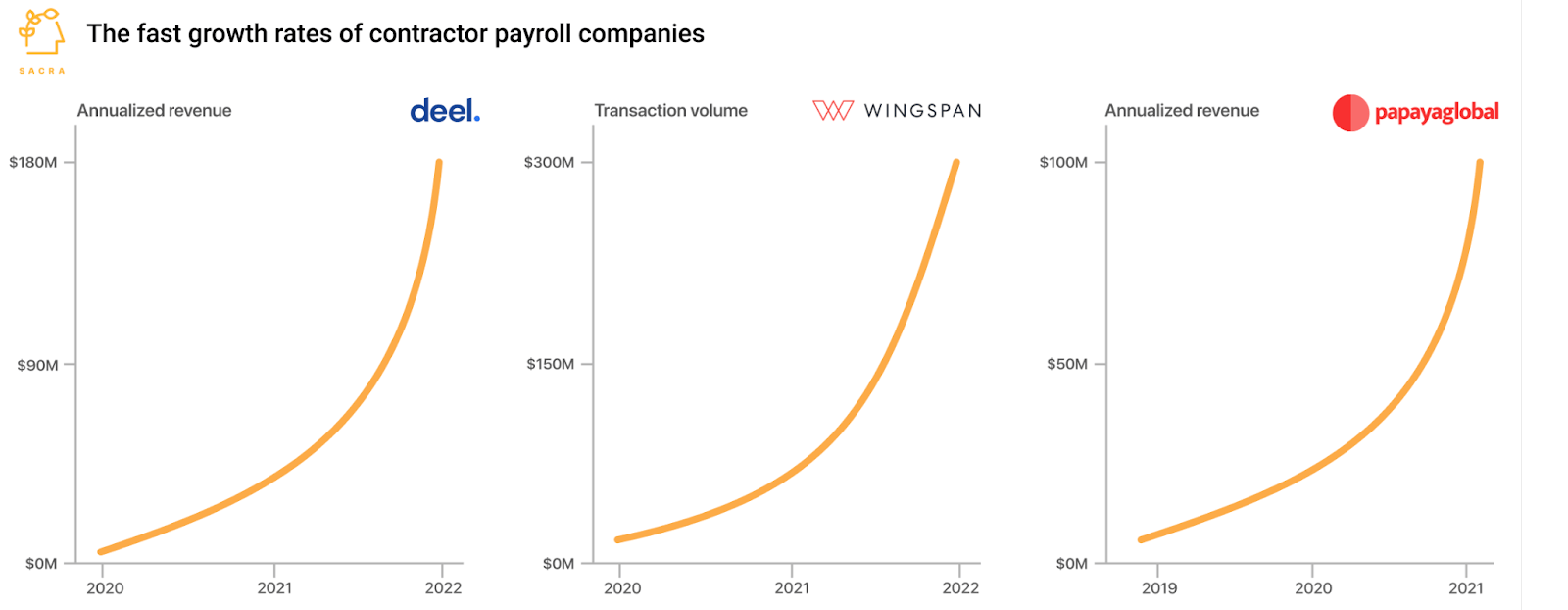

- Deel started 2021 with $4M of ARR. They’ve 45x’ed revenue since then, now doing about $180M.

- Wingspan was doing about half a million in annualized transaction volume in April 2020. As of June 2022, they’re doing $300M.

- Papaya Global hit $100M ARR by the end of 2021 after growing revenue 300% each of the preceding two years.

With these services, any company of any size can hire anyone in the world as a contractor. They can run payroll across all of them with a single click as easily as they would their regular employee payroll, and they can have the legal and compliance backing to feel confident that they’re doing it the right way.

In this way, Deel and co. opened the door to a new kind of geo-arbitrage of labor: instead of just leveraging the cost of living difference between different places to get cheap gig work or offshore a whole division, companies now had access to a form of low capex global hiring that could allow them them to have a global-first perspective on building their team.

The cost savings on bringing on full-time members of the team as contractors rather than employees are significant: between two 40 hour per week workers with an hourly rate of $60, the employee will have an effective cost of around $130 after insurance, taxes, benefits, and other overhead costs, while the contractor will have an effective cost of $70 per hour.

While COVID accelerated the trend towards this new kind of labor relationship, the tailwinds have been there for decades:

- Global talent has been on the rise: India is projected to have more than a million-strong surplus of tech workers by 2030.

- The costs of employment are rising: U.S. healthcare administrative costs are the highest of any advanced economy, and the cost to employers is going up every year

- Cities are getting expensive to hire in: Increasingly, companies are looking outside to the suburbs and rural areas to find affordable labor

Far from a temporary COVID bump, what we’re seeing in the labor market today is part of permanent, secular trends that are going to continue.

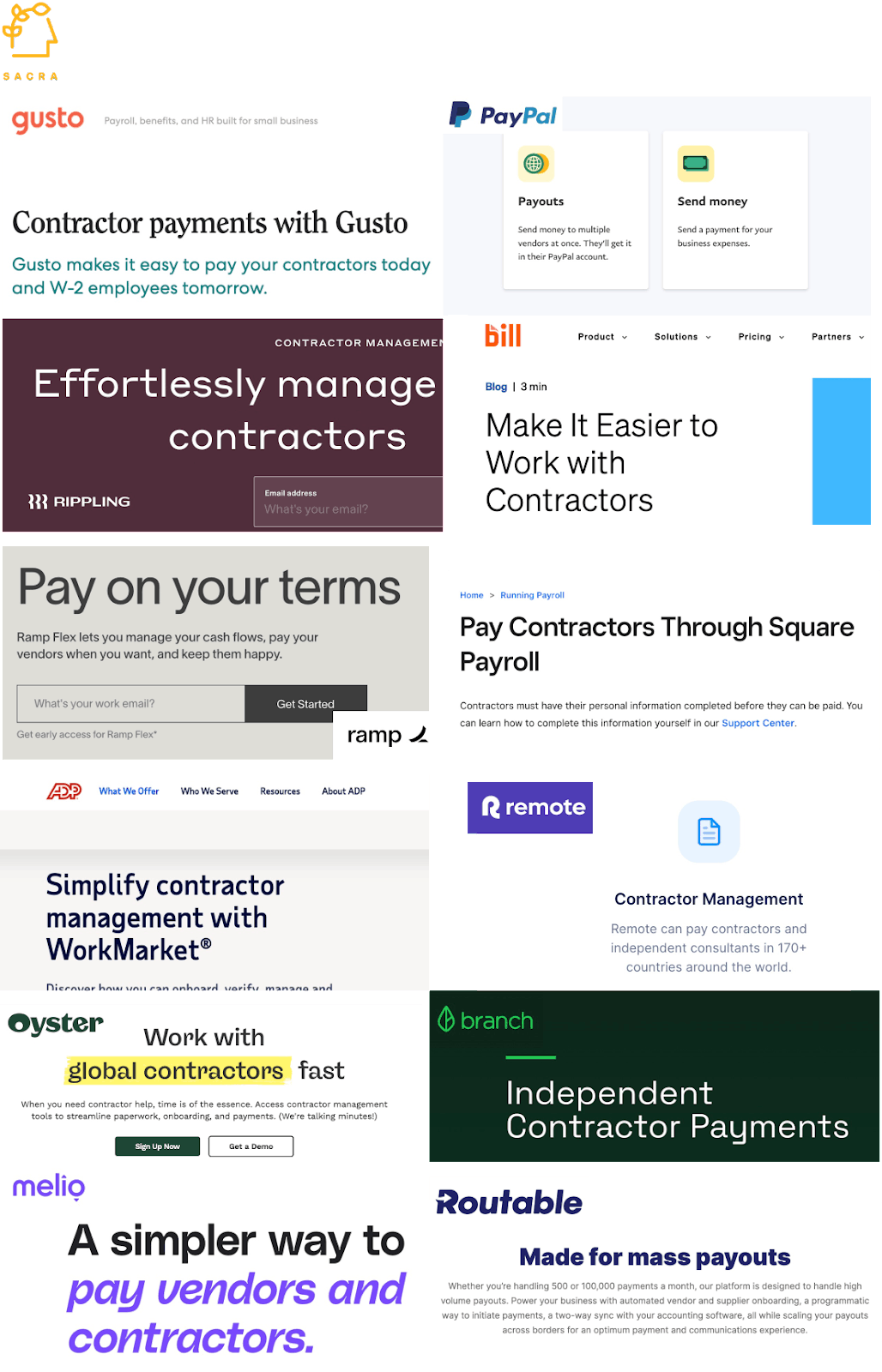

But global payroll companies like Deel and Remote aren’t the only ones that are going after this opportunity: many of the biggest B2B SaaS companies, hoping to own the relationship between contractors and their companies, have been building and launching their own contractor payroll products.

2. Every B2B app from ADP ($96B) to Rippling ($11B), Bill.com ($17B) and Ramp ($8.1B) is bundling contractor payroll

As B2B products all compete to eat up B2B transactions, we’re seeing the widespread bundling of contractor payroll into their products.

These companies want to eat up contractor payroll and include it in the larger bundle of payments and back-office functions they already perform:

- Employee payroll companies like ADP, Paylocity, Paychex, Rippling, and Gusto

- Vertical SaaS like Wingspan, Bonsai, and Toast

- Expense management companies like Bill.com, Brex, and Ramp

- B2B payments businesses like Wise, Square, Melio and Routable

- Payments businesses like PayPal and Venmo

- Global payroll businesses like Deel, Panther, Remote, Oyster, and Papaya Global

Some of these services target different segments of customers. For example, Wingspan primarily targets mid-market companies paying hundreds or thousands of contractors with a particular need for workflow automation around contractor payments—their average ACV on SaaS is around $20K-$70K. Gusto, which is focused on SMB payroll, brings in about $260M a year in revenue on more than 200,000 customers for about $1.3K per customer.

On the other hand, they’re threatened by an emerging set of companies like Check ($119M raised) and Zeal ($15.4M raised) that are abstracting the payroll function into a set of APIs open to any vertical SaaS to use.

Vertical SaaSes want to offer their own payroll functions because doing so adds another layer to their business model with:

- Higher stickiness: When SMBs use vertical SaaSes for payroll, it makes it harder for them to rip that product out in the long term—see ADP’s 91%~ client retention rate for example

- Lower account costs: Companies can lower their account servicing costs by 90% by offering financial services internally rather than relying on 3rd parties

- Increased LTV: Vertical SaaSes that offer payroll to their customers open the door to selling additional financial services, growing their customers’ LTV over time

These payroll APIs effectively threaten to turn the contractor payroll use case into a commodity by giving every vertical SaaS and every work marketplace the power to do its own payments as part of its overall product bundle.

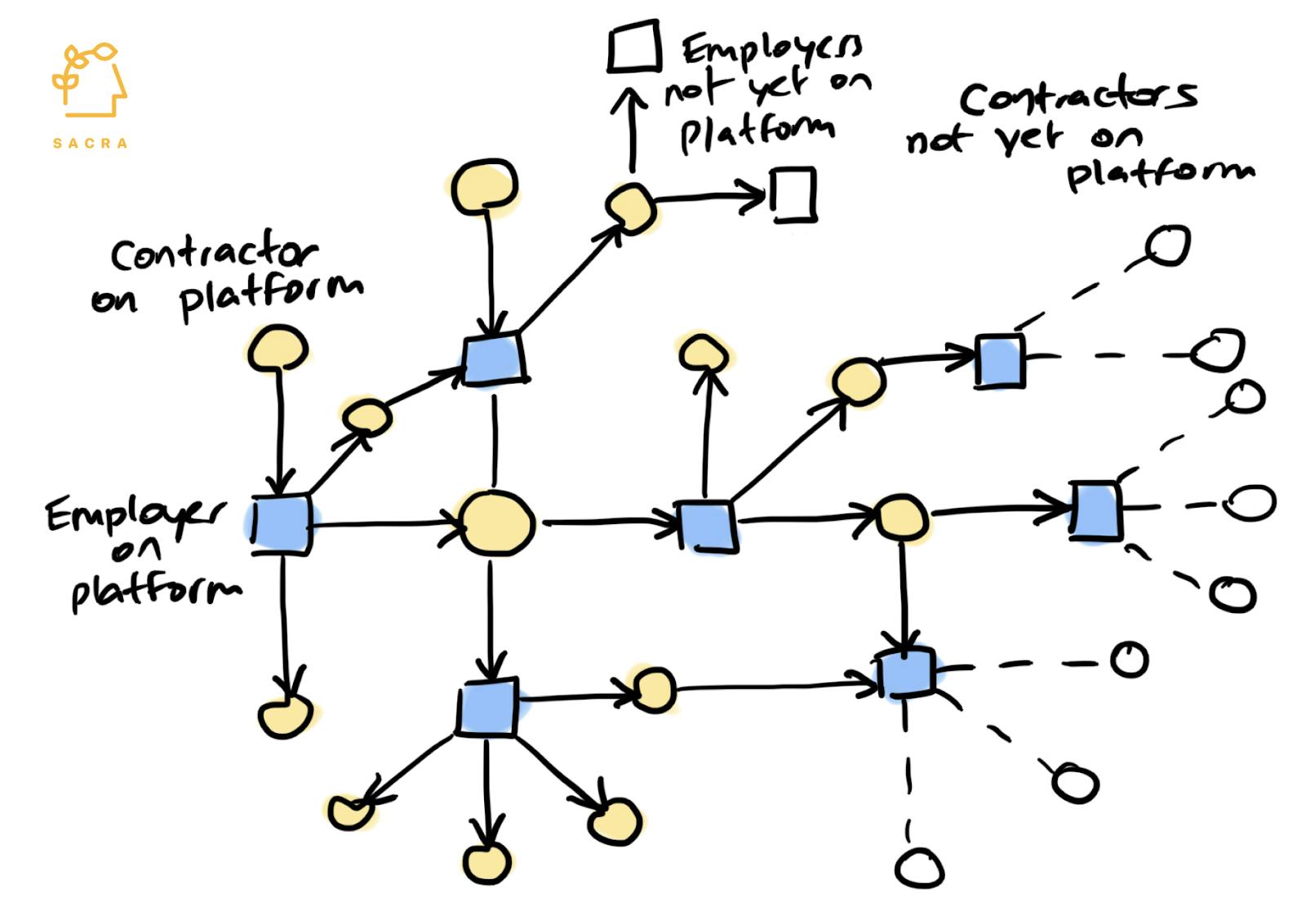

But the big reason all of these different kinds of companies want to own contractor payroll is that while employees are networked via professional graphs like LinkedIn, freelancers are networked via payments graphs.

Companies like ADP, Gusto, Rippling and Ramp want to own the network of contractors not just for cheaper user acquisition but because it is a network with high built-in retention, trillions in fund flows every year, and a long list of monetizable products and services that can be sold into it.

While the average employee only changes jobs once every 4 years, the average contractor works for as many as 12 clients per year. That has created avenues for the networks of contractor payroll platforms to grow larger via each encounter between contractors and companies:

- For contractors, there’s an incentive to have all your clients using the same contractor payroll platform because it simplifies your bookkeeping and your taxes as well as consolidating the wages you earn in your on-platform virtual wallet.

- For companies, there’s an incentive to have all your contractors using the same contractor payroll platform because then you don’t have to collect W9s and do KYC because those contractors will have already gone through that process with the platform.

The problem is that this continued depth of competition creates fragmentation across the payments graph.

Say you’re a contractor and you receive a payment from a company via Bill.com, but you don’t use Bill.com to receive payments. You could make an account, but you’d rather receive payments via the payments app you already use—PayPal, or Wingspan, or Wise.

This kind of fragmentation is widespread in the world of contractor payments today, and it perpetuates its slowness and friction. Companies and clients all have their preferred tools, and because there’s no centralized place where companies and contractors are tracking work together and exchanging funds, contractors have to spend time hunting down and making sure all their invoices have been paid.

This costs contractors money, and makes it harder for them to turn freelancing into a sustainable, full-time source of income.

To win, contractor payroll companies need a value proposition that brings companies and contractors together on one platform—and incentivizes both of them to stick around.

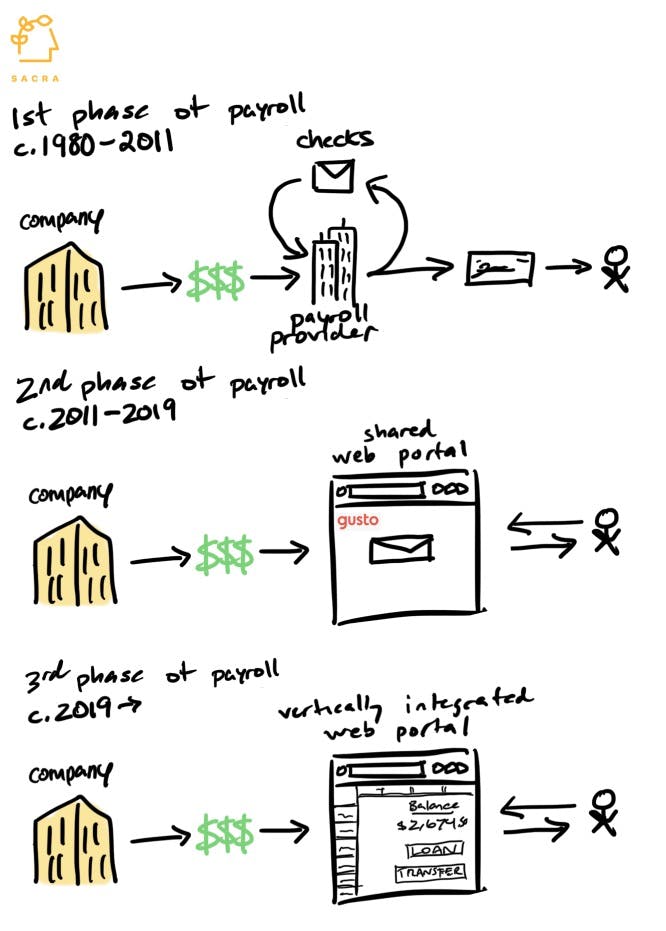

3. Why time-to-money is key to fulfilling contractor payroll’s $1.4T vision

In the first phase of payroll, when it was time to pay your employees, you sent the funds to your payroll processor’s account rep, and they sent back an envelope with physical paper pay stubs.

Gusto changed all of that in the second phase when it moved payroll onto a shared web portal. By bringing companies and employees onto the same platform, Gusto made payroll easier and let employees download their pay stubs, check their benefits, and track their time digitally.

What we’re seeing today is the third phase of payroll:

- Instead of just monetizing on the company, these platforms are monetizing both the company and the employee.

- Instead of being payroll-centric, payroll for these platforms is just a form of leverage to deploy a range of financial services

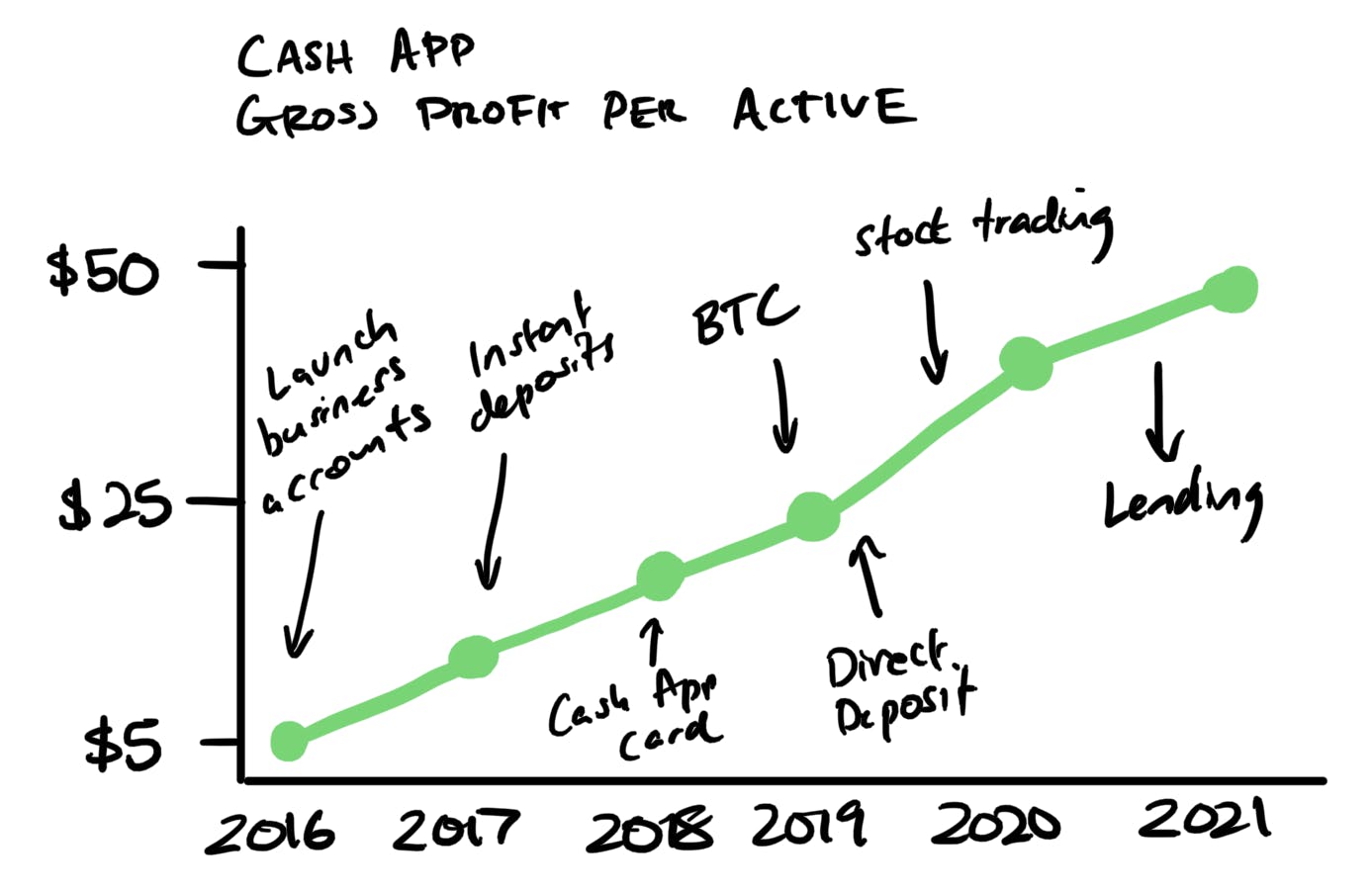

We’ve seen this kind of progression play out before with Square and Cash App.

Cash App (now at $2B a year in gross profit) won over Venmo and other apps by giving users access to their money faster, and they continued to strengthen that time-to-money value proposition over time:

- With Square Cash (launched in 2013): users could instantly receive money sent to them into their debit account

- With the Cash Card (launched in 2017): users could instantly go and spend the money they’d received with a physical debit card—vs. waiting 1-3 business days for ACH

- With Cash App stock trading (launched in 2019): users could instantly go and spend or reinvest money earned from selling stocks—vs. waiting 1-3 business days for ACH

Additional product launches would further strengthen Cash App’s low time-to-money value proposition, make it stickier, and also grow ARPU.

Now, by launching a way for Cash App users to pay Square sellers using Cash App, Block is lurching towards building a closed-loop payments network.

Building a closed-loop network between Cash App users and Square merchants would give them:

- Highly improved unit economics: With a closed network, Block can cut out the 3% cut on all transaction volume that goes to Visa/MasterCard.

- Greater access to data: By working with both merchants and customers, Block can get end-to-end consumer purchasing data they can sell merchants to help sell more and reduce CAC

- Even lower time-to-money: Keeping the money in the loop means Block can offer more financial services to both merchants and users and move funds faster

The big opportunity in contractor payroll is to build a similar closed loop network for the $1.4T and growing of freelancer payments made every year.

Cash App found product-market fit with Americans living paycheck-to-paycheck for whom speed was of the essence because of the potential ripple effects that could arise with any volatility in their personal lives. In the freelancer economy, volatility is the rule, with contractors going from company to company, making their income lumpy and unpredictable.

That has opened up the opportunity for a service that can get money into contractors’ pockets faster, and contractor payroll platforms are perfectly positioned to do that.

Contractor payroll platforms:

- Know how much a particular contractor worked in a day/week, and how much they’re supposed to be paid for it

- Have access to the business’s checking account that they use to pay vendors

- Have access to the contractor’s wallet into which they receive funds

If contractor payroll platforms guaranteed timely freelancer payment based on the amount of work done, it would give contractors a vastly upgraded sense of financial security—and also give their platform the kind of stickiness that Cash App was able to reach in the consumer space by reducing time-to-money in the same way.

By owning the contractor wallet with that 10x better experience, contractor payroll platforms have an opening into selling a range of other products and services into their network. As Gusto built products like Embedded Payroll and Gusto Wallet on top of their network of SMBs, contractor payroll companies have the opportunity to sell things like:

- Freelancer insurance: Liability insurance protects freelancers against claims that they provided the wrong service or their work was faulty in some way

- Contractor loans: Getting a loan as a freelancer can be notoriously difficult, but contractor payroll platforms could more easily underwrite these

- Healthcare and benefits: By acting as a PEO, contractor payroll platforms can get cheaper healthcare for their workers and take that burden off companies

- Earned wage access: Contractor payroll platforms can make earned funds immediately available to contractors for a fee (typically 1%~)

- Talent marketplace: Contractor payroll platforms can allow both companies and contractors to search across their network of workers to staff new projects

Across virtually all of these services, contractor payroll platforms can derive a powerful advantage over other traditional providers by virtue of the data and visibility they have into the activities of both contractors and companies.

The future of contractor payroll

The contractor model offers workers a lot of potential positives: quicker time-to-work than within traditional employment structures, extra income outside an existing job or job search, and greater flexibility—especially important for the inclusion of those with disabilities.

Contractor payroll platforms are fundamentally a bet on the future of this kind of working relationship, and on the upside of the millions of people who are working freelance today and will join the freelance workforce tomorrow.

But to win, contractor payroll platforms will need to beat out stiff competition—not just the other well-capitalized contractor payroll platforms competing for the same turf, but the growing number of vertical SaaS products and gig work marketplaces that are building out their own payroll and workforce management solutions to try and get a slice of what will be trillions of dollars of international fund flows.