Ritz Carlton of vacation rentals

Jan-Erik Asplund

Jan-Erik Asplund

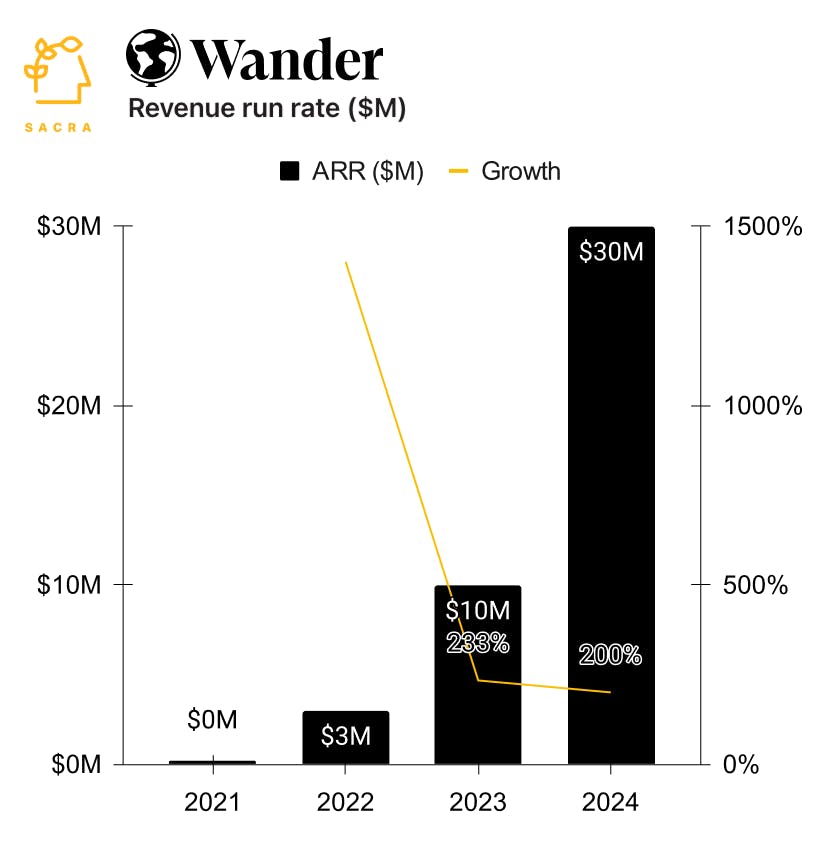

TL;DR: By vertically integrating unique vacation rentals with luxury hotel-like amenities, Wander is betting that it can make the economics of short-term rental (STR) aggregation work where companies like Sonder, Vacasa and Inspirato have struggled. Sacra estimates Wander hit $30M in revenue run rate in 2024, up 200% YoY, as they expanded from 35 to 333 listings through their new asset-light model. For more, check out our full report and dataset on Wander.

Key points via Sacra AI:

- Combining the visual, Instagram-native appeal of Airbnb (which hired professional photographers to enliven vacation rental listings) with the consistency of the hotel experience, Wander launched in 2021 as a vertically-integrated vacation rental company that acquired $2-3M, architecturally-unique properties in vacation hotspots (Big Sur, Joshua Tree), converted them to luxury rentals with hotel-grade amenities and monetized them with a 12% guest fee (compared to Airbnb’s 14%). A consumer marketplace on the front end, on the back end, Wander acquired properties through its Wander Atlas REIT to fund acquisitions ($18M raised, ~7 homes), with another Wander subsidiary responsible for owning, renovating, managing, and eventually selling the properties (targeted 8% annual return).

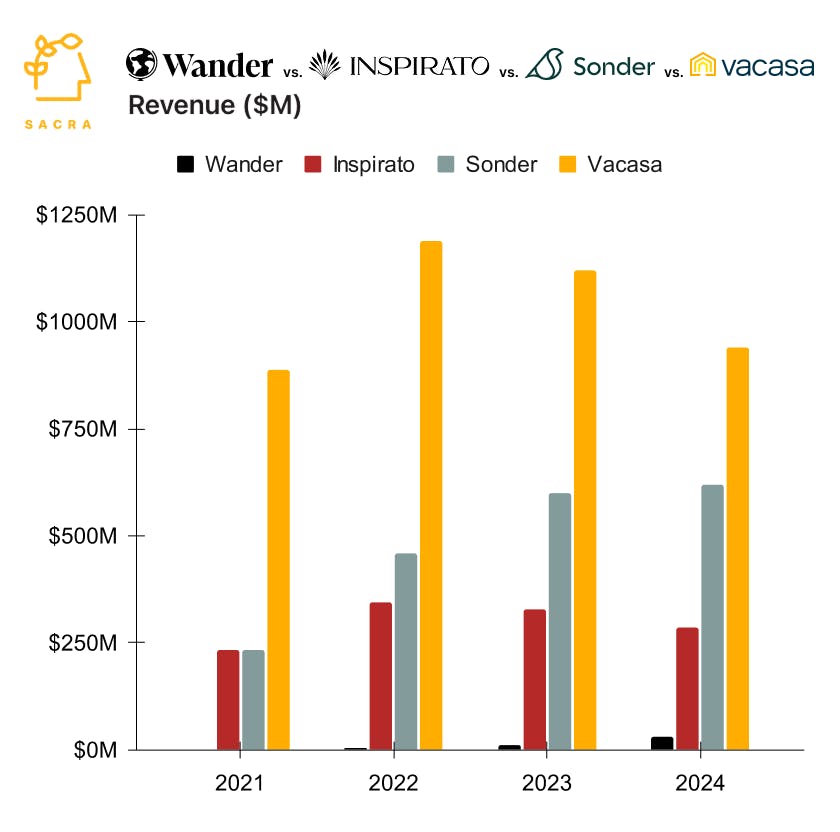

- To scale the supply side from 10 to now 330+ properties, Wander moved in 2023 from its asset-heavy approach to a fully-managed model where it lists and manages properties on behalf of property owners and monetizes through 20-25% revenue share—with Sacra estimating that Wander's annual revenue run rate hit $30M in 2024, up 200% YoY. Compare to other vertically-integrated short-term rental competitors like Inspirato (NASDAQ: ISPOW) at $287M in TTM revenue (down 13% YoY), Sonder (NASDAQ: SOND) at $620M (up 3% YoY), and Vacasa (NASDAQ: VCSA) at $940M (down 16% YoY), which have struggled with profitability amid declining occupancy rates (Vacasa, ~40%), low revenue per available room (Sonder, ~$150) and high operating costs (Inspirato, 25% gross margin in 2023).

- The upside case for Wander is that by aggregating the supply of the top 1% of vacation rentals, they can drive predictable high-value bookings through their own channel (80% of bookings are direct vs. ~50% for Sonder), maximizing their pricing power (33% higher average daily rate than competitors) and funding the strong management services necessary to drive repeat business. The challenge is that Wander’s differentiated supply of unique, remote properties makes it hard to drive efficiencies across cleaning, maintenance, and guest support—unlike regional/urban-focused providers which serve dense clusters of properties in close proximity.

For more, check out this other research from our platform:

- Wander (dataset)

- Tyler Scriven, CEO of Saltbox, on co-warehousing and D2C ecommerce

- Mike Yu, CEO of Vesta, on building a new system of record for the mortgage industry

- WeWork: Behind Their Overpriced $9B SPAC [2021]

- WeWork: How the $3.5B Flex Space Giant is Engineering A Comeback [2020]

- Snapdocs

- Notarize

- Jordan Gonen, CEO of Compound, on software-enabled wealth management

- Compound, Savvy, and the Mint for the 0.1%

Read more from

Wander revenue, growth, and valuation

Unlocked Report

Continue Reading

Read more from

Bilt revenue, growth, and valuation

Unlocked Report

Continue Reading