Revenue

$1.40B

2024

Funding

$4.80M

2024

Growth Rate (y/y)

20%

2023

Revenue

Click here to access our OnlyFans dataset.

OnlyFans generated $1.4B in revenue in 2024, up 7% year-over-year from $1.3B in 2023 on about $7.2B in gross payments volume. The platform recorded pre-tax profit of about $684M in fiscal year 2024.

OnlyFans's biggest revenue generator is the 20% take rate that it collects on each content sale or membership on the platform.

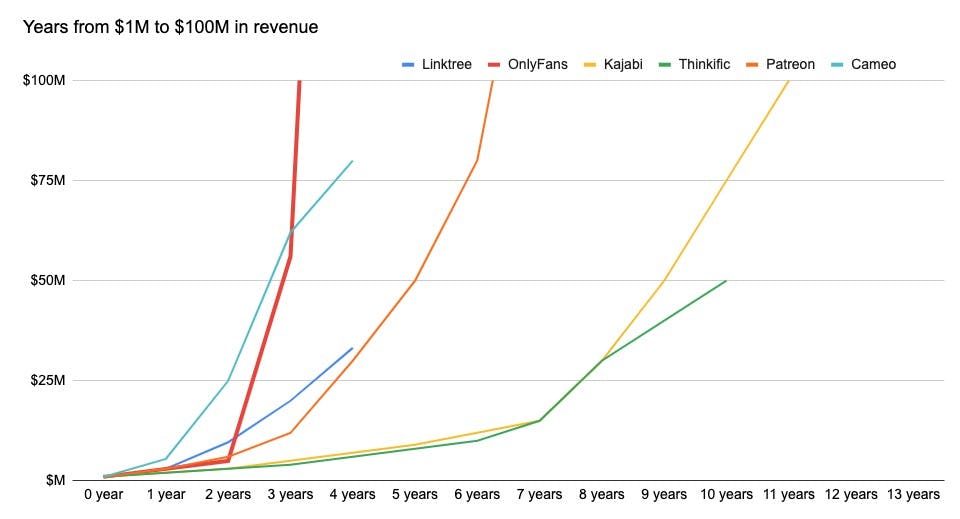

OnlyFans became a cultural phenomenon during COVID, growing from $56M in revenue to nearly $1B over the 2020-1 lockdown period when there was a hiatus on entertainment production, including professional porn.

In October 2025, OnlyFans CEO Keily Blair said the platform has paid out $25B to creators since 2016.

Valuation & Funding

As of May 2026, OnlyFans sold a 16% minority stake to San Francisco-based Architect Capital at a $3.15B valuation. This follows earlier deal terms reported in January 2026 under which Architect was in exclusive talks to acquire close to 60% of the business at a $5.5B enterprise valuation (including ~$2B in debt, with equity valued at ~$3.5B), and a May 2025 process led by Forest Road Co. at an ~$8B valuation that did not result in a transaction.

OnlyFans is owned by Ukrainian-American entrepreneur Leonid Radvinsky through parent company Fenix International, after he bought a majority stake in 2018 from the platform's British founders. The company has no external financing and no debt, and has paid $497M in ordinary dividends to Radvinsky in FY2024 (vs. $472M in FY2023), with an additional $204M in dividends declared between December 2024 and April 2025—$701M in total dividends tied to the period.

Product

OnlyFans is fundamentally an Instagram-like social media platform built around the idea of paywalled interactive content subscriptions rather than a feed of content from your friends.

Designed to give fitness influencers, reality stars and travel bloggers an easier way to monetize their followings via subscriptions, OnlyFans found product-market fit with NSFW creators with its 20% take rate (vs. the 40% charged by sites like MyFreeCams).

OnlyFans has built the biggest and most trusted brand in their space—the Coinbase of amateur porn—backed by bank-grade KYC/AML to verify creator identities and human monitoring of all content and messaging, fostering good relationships with law enforcement and regulators.

Today OnlyFans is about 3x as big as Pornhub parent company MindGeek (~$450M in 2022, and flat since 2018)—which Visa and Mastercard demonetized amid concerns about revenge porn and CSAM being uploaded anonymously to the site.

As a fan, once you subscribe to a performer on the platform, you’re able to view their feed, see additional content available to purchase, send them DMs, and interact with other members of their community.

As a performer, you can use the OnlyFans back-end to set your own prices for your subscription, create different tiers of service, message some or all of your fans, and upload and create photos and videos.

A statistics page allows performers to see their growth over time and assess how different kinds of content are working for conversion and engagement.

Business Model

OnlyFans is a subscription-based content platform that enables creators to monetize their fan base through monthly subscriptions and pay-per-view content. The company generates revenue by taking a 20% cut of all earnings on the platform, with creators keeping 80%. OnlyFans has paid out $25B to creators since its founding in 2016.

In FY2024 (year ended November 30, 2024), OnlyFans generated $1.413B in revenue (up 8.1% from $1.307B) on $7.216B in gross site volume (up 8.8%), with $683.6M in pre-tax profit and $520.3M in net profit. The platform had 4.634M creator accounts and 377.456M fan accounts, up 13% and 24% year over year respectively. The company held $808.1M in cash and generated $591.5M in operating cash flow, with no external debt.

Creators set their own subscription prices, ranging from $4.99 to $49.99 per month, with the average around $7.21. They can also offer pay-per-view content, typically charging $5-10 per minute for videos or $5+ per image. The parasocial relationships fostered between creators and fans drive ongoing subscriptions and additional purchases of pay-per-view content, with tips and custom content requests creating additional revenue streams for both creators and the company.

Competition

OnlyFans' reliance on creators bringing traffic from external social media is both a strength and weakness. It allowed for rapid scaling but makes the platform vulnerable to competitors—creators can easily swap out their OnlyFans link on their Linktree for a rival platform, whether a membership platform or a SFW alternative to OnlyFans.

Membership platforms

In the broad scope of content, OnlyFans competes with other membership-based creator economy platforms like Fanhouse, Patreon, Substack, and Buy Me A Coffee.

Fanhouse is the closest to OnlyFans in terms of its emphasis on the feed and sharing photo and video content, although a key difference is that they forbid all explicit adult or nude content in their terms of service—instead, “performers” share content like vlogs and life updates and participate in group chats with their fans.

Patreon is the largest membership site competitor to OnlyFans, with roughly 8M+ patrons and more than 250,000 creators on the platform. Patreon cracked down on adult content in 2017 amid pressure from payment partners but has since loosened up—today, mature content marked “Patron Only” is accepted on the platform.

Adult content sites

Within the adult entertainment industry, OnlyFans competes with established tube sites like Pornhub (owned by MindGeek) and newer creator-focused platforms like Fansly.

OnlyFans has positioned itself as a more ethical alternative to tube sites, with stringent creator verification processes and better revenue sharing.

It generated about 3x the revenue of Pornhub's parent company MindGeek in 2023 ($1.3 billion vs. ~$450 million). However, competitors like Fansly are gaining traction by offering better internal discovery features for smaller creators, potentially peeling off market share from OnlyFans.

SFW creator platforms

A new category of competition has emerged in the form of safe-for-work (SFW) creator platforms like Passes and Sunroom.

These platforms aim to attract a wider base of influencers and models by taking a smaller cut of earnings (e.g., Passes takes 10% vs. OnlyFans' 20%) and maintaining a no-nudity policy.

This positioning allows them to classify as lower-risk merchants with banks, potentially benefiting their cost structure. While these platforms don't directly compete for OnlyFans' core adult content creators, they could appeal to mainstream influencers and celebrities who might otherwise consider OnlyFans for monetization.

TAM Expansion

With 8.1% revenue growth in FY2024, OnlyFans at $1.413B in revenue has decelerated materially from 17% growth in 2022 and 20% in 2023, reflecting the challenges of scaling beyond its core adult content base.

OnlyFans's ability to go upmarket and expand their TAM is limited by their NSFW positioning—creators on OnlyFans lose out on more mainstream opportunities like brand deals, modeling contracts or appearing in Netflix shows, unlike with SFW upstarts like Passes.

SFW content

One key area of potential TAM expansion for OnlyFans hinges on getting beyond explicit adult content. OnlyFans's aim is for their site to be the core membership platform of the creator economy for everyone from fitness influencers to chefs to comedians.

OFTV, the YouTube-like streaming platform launched in August 2021, has shown early signs of mainstream crossover—its licensed content reached Netflix UK and an original production won a UK National Reality TV Award. OnlyFans has also expanded its comedy vertical through its LMAOF program, and entered sports and entertainment via a major sponsorship and content partnership with DAZN and a partnership with the Professional Fighters League.

Generative AI

As AI gets better, OnlyFans has the opportunity to integrate AI-powered features to enhance user experiences and creator productivity. This could include AI chatbots to handle routine fan interactions and personalized content recommendations to increase engagement and spending. OnlyFans could also explore AI-generated content as a complementary offering, including personalized AI avatars, opening up new creative possibilities and potentially attracting users interested in AI-human interactions.

Risks

Regulatory backlash: Ofcom fined Fenix International £1.05M for misrepresenting its age-assurance measures — its facial estimation tool had been configured to challenge users at age 20 since 2021, not age 23 as previously described to the regulator. Any further failures in content moderation or regulatory disclosure could trigger payment processor restrictions similar to what Pornhub faced, severely impacting revenue.

Ownership transition: Leonid Radvinsky, who controlled the company through Fenix International after acquiring a majority stake in 2018, died weeks before the Architect Capital stake sale closed, leaving a closely-held platform with no external board facing material uncertainty around governance, succession, and strategic direction.

AI-driven commoditization: The rise of AI chatbots and content generation tools threatens to commoditize the personalized interactions that drive OnlyFans' retention and monetization. As AI becomes more sophisticated at simulating intimate conversations, it could reduce subscriber willingness to pay and undermine overall platform engagement.

News

DISCLAIMERS

This report is for information purposes only and is not to be used or considered as an offer or the solicitation of an offer to sell or to buy or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting or tax advice or a representation that any investment or strategy is suitable or appropriate to your individual circumstances or otherwise constitutes a personal trade recommendation to you.

This research report has been prepared solely by Sacra and should not be considered a product of any person or entity that makes such report available, if any.

Information and opinions presented in the sections of the report were obtained or derived from sources Sacra believes are reliable, but Sacra makes no representation as to their accuracy or completeness. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a determination at its original date of publication by Sacra and are subject to change without notice.

Sacra accepts no liability for loss arising from the use of the material presented in this report, except that this exclusion of liability does not apply to the extent that liability arises under specific statutes or regulations applicable to Sacra. Sacra may have issued, and may in the future issue, other reports that are inconsistent with, and reach different conclusions from, the information presented in this report. Those reports reflect different assumptions, views and analytical methods of the analysts who prepared them and Sacra is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report.

All rights reserved. All material presented in this report, unless specifically indicated otherwise is under copyright to Sacra. Sacra reserves any and all intellectual property rights in the report. All trademarks, service marks and logos used in this report are trademarks or service marks or registered trademarks or service marks of Sacra. Any modification, copying, displaying, distributing, transmitting, publishing, licensing, creating derivative works from, or selling any report is strictly prohibited. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of Sacra. Any unauthorized duplication, redistribution or disclosure of this report will result in prosecution.