Revenue

$200.00M

2021

Valuation

$3.00B

2022

Funding

$525.00M

2022

Growth Rate (y/y)

100%

2022

Valuation: $3.00B in 2022

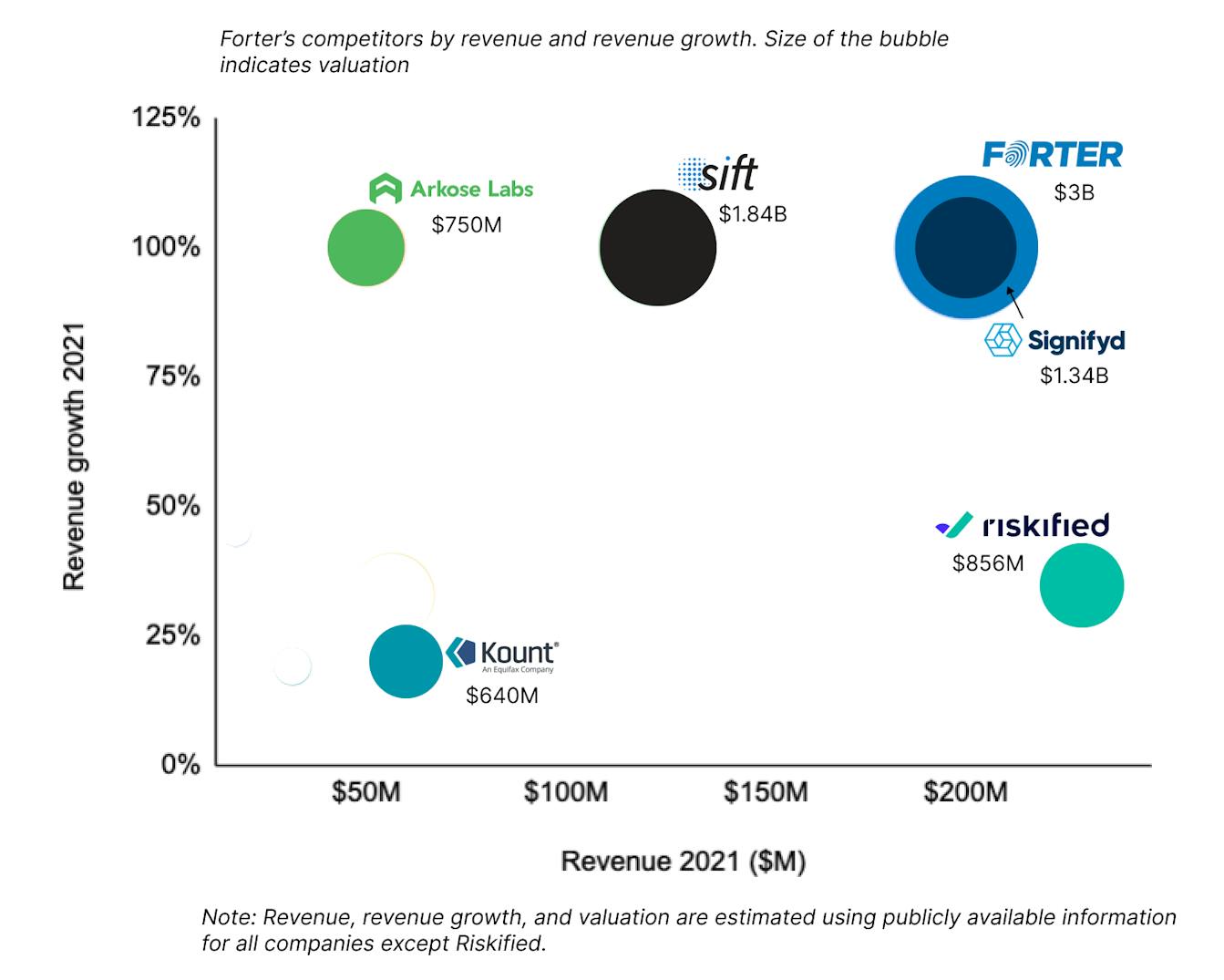

Forter has raised $525 million from investors such as Bessemer Venture Partners and Sequoia Capital. It was last valued at $3 billion, making it one of the most valuable companies in the online fraud detection market. One of its closest publicly listed competitors, Riskified, has a market cap of $856 million with a revenue of $229 million. Its valuation/revenue multiple is 3.7—less than four times that of Forter. Another significant competitor Sift is valued at $1.84 billion with a revenue of $122 million.

Forter's competitors by revenue and revenue growth. Bubble size indicates valuation. Figures estimated using publicly available information.

Scenarios: $971M to $13.9B ARR by 2026

To evaluate Forter's potential future value, we've developed scenarios based on different growth rates and revenue multiples through 2026. These projections consider various market conditions, competitive dynamics in the fraud detection space, and possible company performance trajectories.

| 2021 Revenue ($M) | $200M | ||

|---|---|---|---|

| 2021 Growth Rate (%) | 100.00% |

Forter demonstrated remarkable growth in 2021, doubling its revenue to $200M while processing $250B in GMV. This 100% year-over-year expansion reflects strong market penetration and positions the company as a leading player in the fraud detection space.

| Multiple | Valuation |

|---|---|

| 1x | $200M |

| 5x | $1B |

| 10x | $2B |

| 15x | $3B |

| 25x | $5B |

Based on Forter's $200M revenue, valuations span from $200M at a conservative 1x multiple to $5B at an ambitious 25x multiple. The company's current $3B valuation implies a 15x multiple, positioning it between established competitors like Riskified (3.7x) and high-growth tech valuations.

| 2026 Growth Rate | 2021 | 2022 | 2023 | 2024 | 2025 | 2026 |

|---|---|---|---|---|---|---|

| 10.0% | $200M | $352M | $545M | $731M | $883M | $971M |

| 20.0% | $200M | $357M | $571M | $808M | $1B | $1.3B |

| 30.0% | $200M | $362M | $598M | $890M | $1.2B | $1.6B |

| 55.0% | $200M | $376M | $667M | $1.1B | $1.8B | $2.8B |

| 100.0% | $200M | $400M | $800M | $1.6B | $3.2B | $6.4B |

| 110.0% | $200M | $405M | $831M | $1.7B | $3.6B | $7.6B |

| 120.0% | $200M | $411M | $863M | $1.9B | $4B | $8.9B |

| 135.0% | $200M | $419M | $911M | $2.1B | $4.7B | $11.1B |

| 150.0% | $200M | $427M | $961M | $2.3B | $5.5B | $13.9B |

Based on different growth scenarios, Forter's revenue could range from $971M at a conservative 10% growth rate to $13.9B at an aggressive 150% growth rate by 2026. The projections demonstrate substantial upside potential from the 2021 baseline of $200M, particularly if the company maintains its strong growth trajectory.

| 2026 Growth Rate | 1x | 5x | 10x | 15x | 25x |

|---|---|---|---|---|---|

| 10.0% | $971M | $4.9B | $9.7B | $14.6B | $24.3B |

| 20.0% | $1.3B | $6.3B | $12.6B | $18.8B | $31.4B |

| 30.0% | $1.6B | $8B | $16B | $24B | $40B |

| 55.0% | $2.8B | $13.9B | $27.7B | $41.6B | $69.3B |

| 100.0% | $6.4B | $32B | $64B | $96B | $160B |

| 110.0% | $7.6B | $37.8B | $75.5B | $113.3B | $188.9B |

| 120.0% | $8.9B | $44.3B | $88.6B | $132.9B | $221.6B |

| 135.0% | $11.1B | $55.7B | $111.5B | $167.2B | $278.7B |

| 150.0% | $13.9B | $69.3B | $138.6B | $207.9B | $346.6B |

Based on varying growth scenarios and revenue multiples, Forter's 2026 valuations could range from $971M (10% growth, 1x multiple) to $346.6B (150% growth, 25x multiple). The wide spread reflects both the company's significant growth potential and the uncertainty inherent in long-term projections.

Bear, Base, and Bull Cases: 5.5x, 7.5x, 9.5x

To provide a nuanced perspective on Forter's potential trajectories, we've developed bear, base, and bull case scenarios using multiples of 5.5x, 7.5x, and 9.5x respectively. These cases account for market dynamics, competitive pressures, and Forter's execution capabilities in the fraud prevention space.

| Scenario | 2026 Growth Rate (%) | Multiple |

|---|---|---|

| Bear 🐻 | 20% | 5.5 |

| Base 📈 | 90% | 7.5 |

| Bull 🚀 | 150% | 9.5 |

Growth projections range significantly across scenarios, from a conservative 20% growth rate with 5.5x multiple in the bear case, to a robust 90% growth with 7.5x multiple in the base case, to an ambitious 150% growth and 9.5x multiple in the bull case, reflecting the range of potential outcomes in the fraud prevention market.

| Bear 🐻 | 2021 | 2022 | 2023 | 2024 | 2025 | 2026 |

|---|---|---|---|---|---|---|

| Revenue | $200M | $357M | $571M | $808M | $1B | $1.3B |

| Growth | 100.00% | 78.48% | 60.00% | 41.52% | 29.54% | 20% |

| Base 📈 | 2021 | 2022 | 2023 | 2024 | 2025 | 2026 |

|---|---|---|---|---|---|---|

| Revenue | $200M | $395M | $770M | $1.5B | $2.8B | $5.4B |

| Growth | 100.00% | 97.31% | 95.00% | 92.69% | 91.19% | 90% |

| Bull 🚀 | 2021 | 2022 | 2023 | 2024 | 2025 | 2026 |

|---|---|---|---|---|---|---|

| Revenue | $200M | $427M | $961M | $2.3B | $5.5B | $13.9B |

| Growth | 100.00% | 113.45% | 125.00% | 136.55% | 144.04% | 150% |

Our bear, base, and bull cases for Forter reflect varying trajectories based on competitive dynamics and market penetration in the fraud prevention space

- In the bear case, regulatory changes and competitive pressures lead to a $6.9B valuation by 2026, with revenue reaching $1.3B at a compressed 5.5x multiple and slowed growth of 20%

- In the base case, Forter maintains its strong market position to reach a $40.4B valuation, with revenue growing to $5.4B at a 7.5x multiple and 90% growth rate

- In the bull case, Forter's expansion into new verticals and AI capabilities drives a $131.7B valuation, with revenue soaring to $13.9B at a premium 9.5x multiple and 150% growth rate.

| Scenario | 1. Bear 🐻 | 2. Base 📈 | 3. Bull 🚀 |

|---|---|---|---|

| 2021 Revenue | $200M | $200M | $200M |

| 2021 Growth Rate (%) | 100% | 100% | 100% |

| 2021 Multiple | 5.5 | 7.5 | 9.5 |

| 2021 Valuation | $1.1B | $1.5B | $1.9B |

| 2026 Revenue | $1.3B | $5.4B | $13.9B |

| 2026 Growth Rate (%) | 20% | 90% | 150% |

| Multiple | 5.5 | 7.5 | 9.5 |

| 2026 Valuation | $6.9B | $40.4B | $131.7B |

The uncertainty around these three cases depends primarily on regulatory shifts in fraud liability, Forter's ability to maintain its data advantage against payment giants, and whether it can successfully expand beyond e-commerce while leveraging its AI capabilities and $500B+ processed GMV database.

- In the Bear case: Regulatory changes like PSD2 continue to reduce fraud liability for retailers while payment giants like Stripe and Adyen leverage their massive transaction databases to offer superior fraud prevention solutions, forcing Forter to compete primarily on price with a compressed 5.5x multiple.

- In the Base case: Forter maintains its strong position in e-commerce fraud prevention through its data flywheel advantage and successful expansion into identity management and policy abuse prevention, supporting a 7.5x multiple in line with high-growth SaaS companies.

- In the Bull case: Forter leverages its industry-leading $500B+ processed GMV database and AI capabilities to become the dominant platform for integrated fraud prevention across the entire user journey, while expanding into new verticals beyond e-commerce, justifying a premium 9.5x multiple.

These final valuations present a wide range of potential outcomes for Forter. The bear case projects a $6.9B valuation by 2026, while the base case reaches $40.4B. The bull case at $131.7B would position Forter as a dominant player in fraud prevention technology.

DISCLAIMERS

This report is for information purposes only and is not to be used or considered as an offer or the solicitation of an offer to sell or to buy or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting or tax advice or a representation that any investment or strategy is suitable or appropriate to your individual circumstances or otherwise constitutes a personal trade recommendation to you.

This research report has been prepared solely by Sacra and should not be considered a product of any person or entity that makes such report available, if any.

Information and opinions presented in the sections of the report were obtained or derived from sources Sacra believes are reliable, but Sacra makes no representation as to their accuracy or completeness. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a determination at its original date of publication by Sacra and are subject to change without notice.

Sacra accepts no liability for loss arising from the use of the material presented in this report, except that this exclusion of liability does not apply to the extent that liability arises under specific statutes or regulations applicable to Sacra. Sacra may have issued, and may in the future issue, other reports that are inconsistent with, and reach different conclusions from, the information presented in this report. Those reports reflect different assumptions, views and analytical methods of the analysts who prepared them and Sacra is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report.

All rights reserved. All material presented in this report, unless specifically indicated otherwise is under copyright to Sacra. Sacra reserves any and all intellectual property rights in the report. All trademarks, service marks and logos used in this report are trademarks or service marks or registered trademarks or service marks of Sacra. Any modification, copying, displaying, distributing, transmitting, publishing, licensing, creating derivative works from, or selling any report is strictly prohibited. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of Sacra. Any unauthorized duplication, redistribution or disclosure of this report will result in prosecution.