Revenue

$1.30B

2025

Funding

$360.17M

2021

Revenue

Sacra estimates that CloudWalk hit $1.3B in annualized revenue in 2025, up 131% year-over-year from $562M in 2024.

Revenue is driven primarily by InfinitePay's merchant acquiring business in Brazil, where CloudWalk earns fees on card transactions and monetizes an expanding stack of adjacent fintech products.

Management attributes a material share of growth to newer product lines launched over the prior two years, including working-capital credit, Pix instant payments, and automated fee negotiation.

InfinitePay's seller base reached 3M at the end of 2024 before nearly doubling to 6M within the following nine months, and the company reported $404M in net revenue and $39M in net income in the first half of 2025, implying $128M in annualized net profit by September.

Valuation & Funding

CloudWalk's most recent disclosed round was a $150M Series C closed in November 2021, led by Coatue Management, following a $190M Series B in May 2021 also led by Coatue, bringing total lifetime equity funding to approximately $365M.

Investors across the two rounds included DST Global, FIS, The Hive Brazil, Valor Capital Group, A-Star, Plug and Play Ventures, and angel investor Gokul Rajaram.

Product

CloudWalk runs two merchant-facing brands on a shared payments and AI stack: InfinitePay in Brazil and JIM.com in the United States.

InfinitePay

InfinitePay is CloudWalk's primary product, built for the roughly 10 million Brazilian micro-entrepreneurs (hairdressers, street vendors, delivery drivers) who were paying 5% fees on card transactions and waiting 30 or more days for settlement before it existed.

You download the app, complete a selfie-based ID check, and have a fully functional business account within minutes, with no bank intermediary required.

From there, you accept payments however your customers pay.

You can buy a low-cost card terminal, or skip hardware entirely and use InfiniteTap, which turns your existing iPhone or Android into a contactless point-of-sale.

For remote sales, you send a checkout link, set up a recurring invoice, or embed an InfinitePay checkout on your website. Pix and boleto payments are free. Money hits your account the next business day by default, or immediately via Nitro if you need it now.

Beyond payments, InfinitePay functions as a full financial account.

CloudWalk uses your own transaction history to underwrite a working-capital loan collateralized by your card receivables, so approval is faster and terms are better than a traditional bank.

Idle cash earns above the CDI benchmark rate in an in-app certificate of deposit you can redeem same-day.

Spending on your InfinitePay card earns cashback paid in BRLC, CloudWalk's Brazilian real-pegged stablecoin that settles in six seconds on Stratus, CloudWalk's in-house blockchain.

JIM.com

JIM.com is the U.S. version of InfinitePay, built for nano-merchants like mobile barbers, private tutors, & pop-up shop sellers who run their entire business from a phone.

You download the app, tap to accept a card payment, and the money hits your account the same day, at a flat 1.99% per transaction versus Square's 2.6% plus 10 cents.

The difference from Square is JIM, the AI agent built into the app. Instead of logging into a dashboard to check sales or update your prices, you tell JIM what you need: pull last week's revenue, raise prices by 10%, post a promotional story to Instagram.

JIM has direct access to your point-of-sale and marketing APIs, so it executes the task rather than walking you through how to do it yourself.

Business Model

CloudWalk is a vertically integrated B2C fintech that sells directly to small and micro merchants, with a product stack spanning card acquiring, banking, credit, and AI tooling.

The primary revenue engine is the merchant discount rate (MDR) charged on each card transaction processed through InfinitePay, with debit transactions running around 0.75% and single-installment credit transactions around 2.69%, placing CloudWalk at the low end of the Brazilian acquiring market.

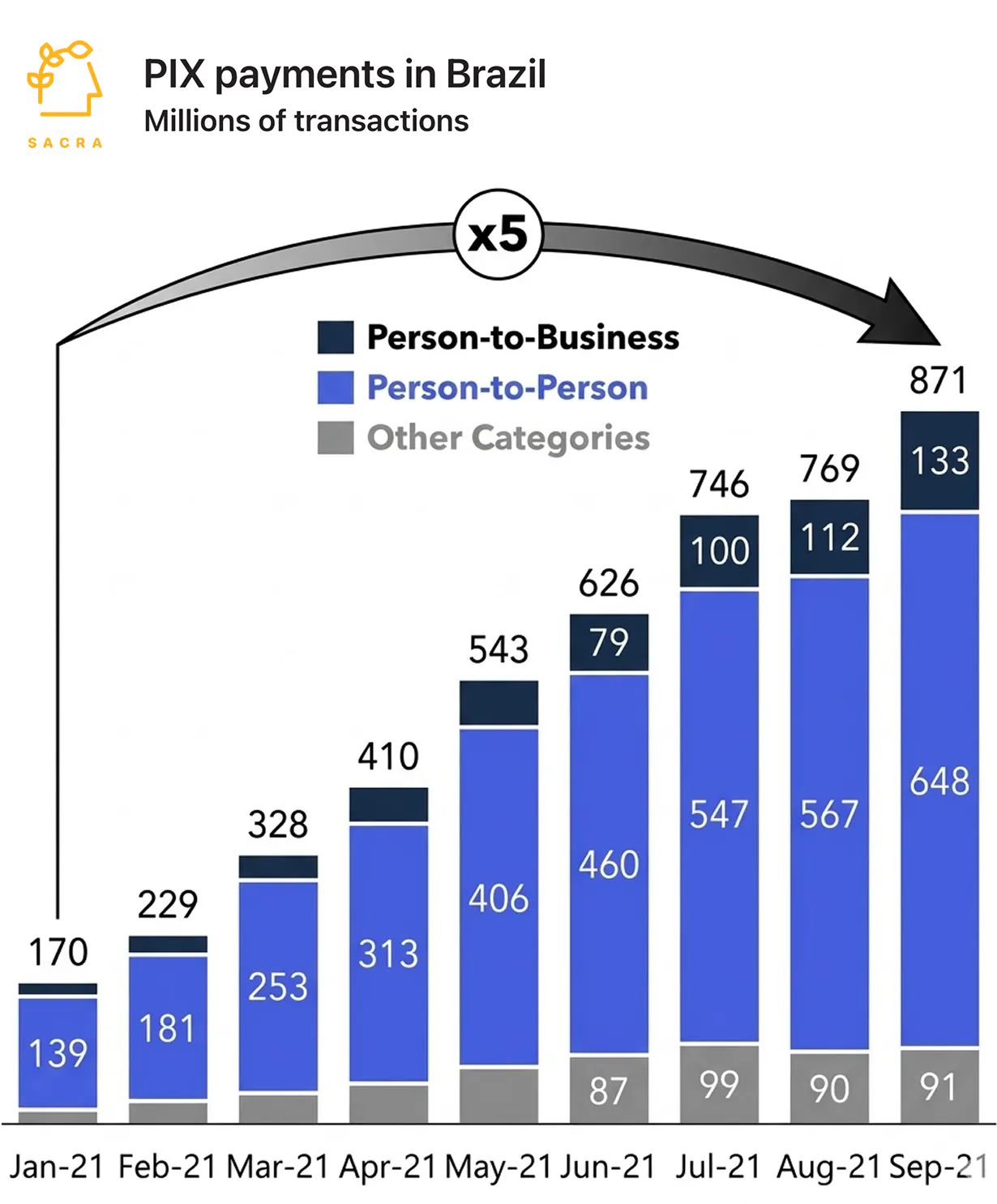

Rather than fight potentially disruptive technologies in stablecoins and Pix, Brazil's instant payment rail that reached 47% of non-cash payment volume in 2024 at merchant costs of 0.22% versus 2.34% for credit cards, CloudWalk has absorbed them into the platform with the launch of its own Brazilian real-pegged stablecoin (6-second settlement), free unlimited Pix, and Pix Credit in 2024, betting that winning market share on merchant experience and pushing forward digital payments will expand per-merchant revenue as credit, lending, and software are layered on top.

A second revenue layer is Nitro, where CloudWalk buys receivables at a discount and earns a spread, then packages those receivables into FIDCs and sells them to institutional capital markets investors, recycling the capital into new advances.

Working-capital loans follow the same structure, underwritten using CloudWalk's own transaction data, which provides more timely visibility into a merchant's cash flows than banks without real-time access to processing data. The in-app CDB deposit product adds a third layer: by attracting retail savings directly into the InfinitePay ecosystem, CloudWalk lowers its cost of funds for the credit business rather than relying entirely on capital markets.

On the cost side, the asset-light hardware strategy removes the logistics and working-capital burden carried by competitors that manufacture and distribute physical devices. AI automation of sales (via an agent called Bela on WhatsApp) and customer service (via an agent called Claudio Walker) allowed CloudWalk to nearly double revenue per employee in a single year without proportional headcount growth.

The operating loop is direct: more merchants generate more transaction data, which improves credit underwriting, which enables better loan terms, which attracts more merchants and drives higher usage across the full financial suite.

Competition

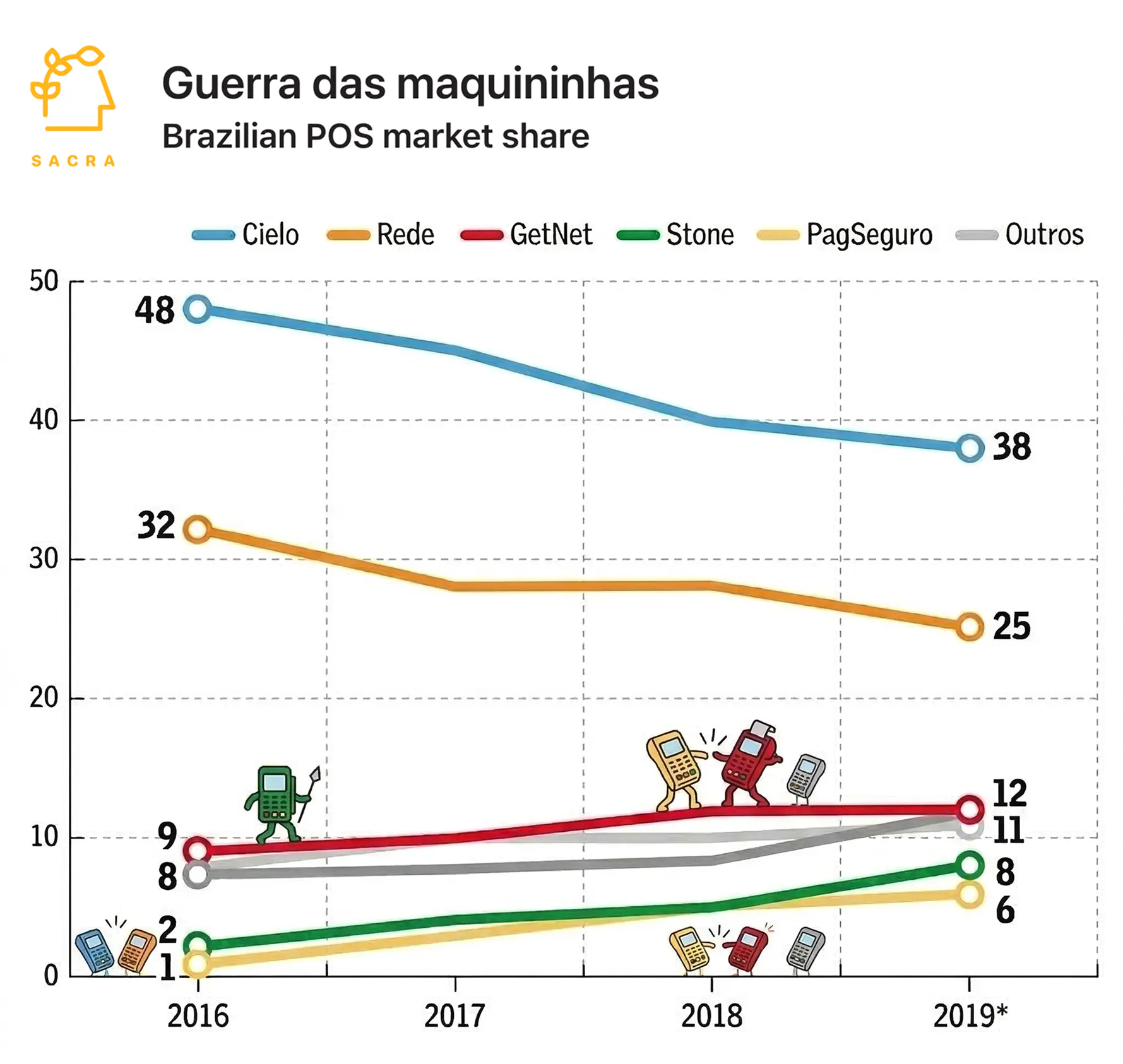

Until 2010, the duopoly of Cielo and Rede, controlling 93% of all card volume, ruled Brazil's merchant acquiring market, charging high take rates and settling merchants in 28-30 days, before regulators broke their brand exclusivity with Visa and Mastercard respectively and triggered the "guerra das maquininhas" (POS war), where insurgents like StoneCo (NASDAQ: STNE, 13% market share) and PagSeguro (NYSE: PAGS, 13% market share) brought card acceptance to millions of previously unbanked small merchants through cheap hardware and lower fees.

Cielo (now roughly 30% market share, $164B volume in 2025) and Rede (roughly 26% market share) fought back by cutting merchant fees and phasing out hardware terminal rental fees, eroding their own margins to protect market share, but merchants still struggled with cash flow, regularly waiting 30 or more days for card proceeds and paying high rates to advance receivables, which is the structural gap CloudWalk's InfinitePay was built to fill.

Vertically integrated Brazilian acquirers

StoneCo and PagSeguro/PagBank are the two most direct structural competitors, both pursuing the same cross-sell model as CloudWalk: acquiring merchants on payments and then layering in credit and banking to increase revenue per customer.

StoneCo serves over 4 million merchants and has rebuilt its economics after the maquininha price wars of the early 2020s by expanding its take rate and restoring return on equity through working-capital credit, banking deposits, and proprietary field-sales distribution, while PagSeguro has moved further into banking, with its PagBank unit reporting banking revenue growth well above 50% year-over-year and launching its first dividend in 2025, signaling a shift from growth-at-all-costs to capital returns.

CloudWalk executes the same model with a fraction of the headcount, using AI agents for functions that Stone and PagSeguro cover with larger field and support teams.

Mobile-first price attackers

SumUp has launched a free Tap-to-Pay product in Brazil with MDR rates competitive with InfinitePay, targeting the same micro-merchant segment. PayPal's Zettle offers global Tap-to-Pay on iOS and Android with overnight settlement and PayPal wallet integration.

These players support CloudWalk's hardware-free thesis but do not offer a full financial stack, with no in-app credit, no deposit product, and no stablecoin settlement layer. That limits stickiness relative to InfinitePay once a merchant is onboarded.

Legacy acquirers and bank-owned networks

Cielo, Rede, and Getnet still control a large share of Brazilian card volume and are backed by the balance sheets of Banco do Brasil, Itau, and Santander respectively. Their pivot toward NFC-only tap products and Pix-enabled terminals indicates a broader shift toward hardware-light acquisition.

The structural risk they pose is on funding cost: bank-owned acquirers can access capital at rates that an independent fintech cannot match, which matters as CloudWalk scales its receivables financing business. Their SaaS-style add-ons and regional sponsorship programs also extend distribution in markets outside major urban centers where InfinitePay's app-first model has less penetration.

U.S. incumbents

In the United States, Square (Block) and Stripe set the competitive baseline for the nano-merchant and SMB segments that JIM.com is targeting. Square's ecosystem, hardware, payroll, banking, and loyalty, is embedded with small retailers. Stripe's developer platform dominates online checkout for businesses that want to build custom payment flows.

CloudWalk's JIM.com differentiates on the AI agent layer: rather than a dashboard the merchant has to manage, JIM executes tasks autonomously. CloudWalk is entering a market where Stripe and Square have years of brand trust, regulatory relationships, and network effects with card networks and banks, advantages that take time and capital to replicate.

TAM Expansion

New financial products

CloudWalk's Pix Credit product, a buy-now-pay-later layer built on top of Brazil's instant payment rail, moves the company from pure acquiring into consumer installment credit. Merchants receive funds immediately while shoppers pay over time, widening CloudWalk's take rate beyond the MDR and accessing Brazil's large annual installment market.

The in-app CDB deposit product adds a second expansion vector: by matching household savings to SME credit inside its own ecosystem, CloudWalk can lower its cost of funds while earning a spread on the intermediation. As the merchant base grows, the deposit pool grows with it, compounding the funding advantage.

AI agents as a platform

The internal AI agents CloudWalk built for its own operations, Bela for WhatsApp-based merchant acquisition and Claudio Walker for customer service, indicate potential to replace portions of traditional fintech headcount. Packaging these agents as plug-ins available to merchants or to outside businesses would create a software revenue line with near-zero marginal cost per additional customer.

JIM, already embedded in InfinitePay and available as a standalone product in the U.S., is the most visible expression of this strategy. A merchant asking JIM to reprice inventory, schedule a promotion, or generate a financial summary interacts with a vertical AI agent for small business operations, a category that Stripe, Square, and Adyen have not yet built in a comparable form.

Geographic and infrastructure expansion

The first major Brazilian fintech to target the U.S. market directly, CloudWalk launched JIM.com in early 2025 as a mobile-first payment platform undercutting Square at a flat 1.99% per transaction (versus Square's 2.6% plus 10 cents), signing up tens of thousands of micro-entrepreneurs across all 50 states and betting that software-only distribution, AI-native operations, and low fees through automated efficiency can transfer to a market where 70 million gig workers face the same pain points of high fees and slow settlement that originally created the opportunity in Brazil.

Stratus, CloudWalk's open-source Ethereum-compatible blockchain, creates a longer-term infrastructure expansion opportunity, giving third-party developers a potential settlement layer for cross-border remittances, tokenized invoices, and other financial products, converting a proprietary internal tool into a horizontal platform with network effects that extend beyond CloudWalk's own merchant base.

Customer base deepening in Brazil

InfinitePay became the most-downloaded finance app on Brazil's App Store in 2025, and the merchant base nearly doubled to 6 million in under a year. The long tail of Brazilian SMBs, street vendors, freelancers, micro-retailers, remains largely underserved by traditional banking infrastructure, and InfinitePay's zero-hardware, app-first model is structurally better suited to reach them than the field-sales models of Stone or PagSeguro.

Each new merchant added to the platform increases the receivables pool available for securitization, the credit data available for underwriting, and the deposit base available for funding, making customer acquisition in Brazil a compounding asset rather than a pure cost.

Risks

FIDC concentration risk: CloudWalk's instant settlement and working-capital lending businesses depend on its ability to continuously securitize merchant receivables through FIDCs and sell them to institutional investors. A deterioration in Brazilian credit markets, a rise in merchant default rates, or reduced demand from FIDC investors could constrain CloudWalk's ability to fund advances, directly limiting the product used for merchant acquisition and retention.

Regulatory exposure: CloudWalk operates under a Central Bank payment institution license in Brazil and is expanding into U.S. financial services, both of which are subject to evolving and sometimes unpredictable regulatory regimes. Brazil's Central Bank has broad authority to modify the rules governing Pix, installment credit, and payment institution capital requirements, any of which could change the unit economics of CloudWalk's core products. In the U.S., state-by-state money transmission licensing and federal oversight of embedded lending increase compliance scope as JIM.com scales.

AI-driven cost structure fragility: CloudWalk's revenue-per-employee ratio is a core element of its cost thesis and operating model, based on the premise that AI agents can replace traditional fintech headcount in sales and support. If the underlying models require more human oversight than currently assumed, due to error rates, regulatory requirements around automated decision-making, or merchant trust issues, the cost advantage could erode faster than the revenue base can absorb it.

News

DISCLAIMERS

This report is for information purposes only and is not to be used or considered as an offer or the solicitation of an offer to sell or to buy or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting or tax advice or a representation that any investment or strategy is suitable or appropriate to your individual circumstances or otherwise constitutes a personal trade recommendation to you.

This research report has been prepared solely by Sacra and should not be considered a product of any person or entity that makes such report available, if any.

Information and opinions presented in the sections of the report were obtained or derived from sources Sacra believes are reliable, but Sacra makes no representation as to their accuracy or completeness. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a determination at its original date of publication by Sacra and are subject to change without notice.

Sacra accepts no liability for loss arising from the use of the material presented in this report, except that this exclusion of liability does not apply to the extent that liability arises under specific statutes or regulations applicable to Sacra. Sacra may have issued, and may in the future issue, other reports that are inconsistent with, and reach different conclusions from, the information presented in this report. Those reports reflect different assumptions, views and analytical methods of the analysts who prepared them and Sacra is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report.

All rights reserved. All material presented in this report, unless specifically indicated otherwise is under copyright to Sacra. Sacra reserves any and all intellectual property rights in the report. All trademarks, service marks and logos used in this report are trademarks or service marks or registered trademarks or service marks of Sacra. Any modification, copying, displaying, distributing, transmitting, publishing, licensing, creating derivative works from, or selling any report is strictly prohibited. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of Sacra. Any unauthorized duplication, redistribution or disclosure of this report will result in prosecution.