Revenue

$4.00B

2025

Valuation

$42.00B

2026

Funding

$572.60M

2025

Growth Rate (y/y)

44%

2025

Revenue

Sacra estimates that Canva hit $4B in ARR at the end of 2025, up 43% from $2.8B at the end of 2024. Canva's own 2025 recap reported $3.5B in revenue for the year, with ARR and recognized revenue diverging as the company scales annual and multi-year contracts.

Monthly active users reached 265M at the end of 2025, up from 180M the year prior, with over 31M paid users. AI usage reached 800M tool uses per month, up 700% year-over-year, with Magic Studio logging more than 24B total uses over the past year.

Canva's B2B business (companies with 25+ seats) reached $500M in ARR with 100% growth, representing approximately 12.5% of total revenue. The company still sees the majority of its business from North America, with continued growth in international markets. To increase paying users, Canva has introduced lower-priced subscriptions in countries like Pakistan, Uruguay, Morocco, and Jamaica.

Valuation & Funding

In August 2025, Canva launched an employee stock sale at a $42B valuation—up more than 30% from its $32B valuation in October 2024—with participation from Fidelity Management & Research and JPMorgan Asset Management.

The company has raised a total of $572.6 million across multiple funding rounds. Key investors include Blackbird Ventures, Sequoia Capital, and General Catalyst.

Business Model

Canva is a subscription SaaS company that primarily prices based on the number of professional/enterprise and productivity features that a team needs—cloud storage, SSO, premium stock photos, post scheduling, and more.

Canva has a strong organic acquisition engine founded on SEO—they rank #1 or near #1 on Google for terms like "ai image generator", "graph maker", "resume templates", "logo maker", "photo editor", "business cards", "tier list maker", and "gif maker".

Farming the free individual users that they acquire through this SEO engine and upselling them to paid plans contracts has been a powerful growth tactic for Canva. With its focus on ease of use and increasingly broad range of use cases, now including videos, Powerpoint-like presentations, and websites, Canva is well set up to bring in free users from every part of the organization—and create maximally fertile ground for upsells. Canva AI being available in 16 languages across 31 locales further extends this PLG motion into non-English markets where the free-to-paid conversion funnel had previously been constrained by language barriers.

Most of Canva's user base is on free, which is by design—Canva wants as many people as possible to use the product.

The Pro plan ($119 per year for one person) is mainly for people that want access to the advanced content library and want to collaborate with more than one fellow creator, or that need more storage—it's mainly a plan for SMBs.

Canva Business, at $20 per person per month with no seat minimum, is the default plan for new team sign-ups and upgrades, replacing Canva Teams. It bundles Canva Grow Insights, higher AI limits, Leonardo.Ai Essential, Flourish Presenter, and a 10% Canva Print discount, with existing Teams subscribers grandfathered into their prior pricing and features.

Product

Canva was founded in 2013 by Melanie Perkins and Cliff Obrecht during the rapid rise of image-based social media.

As Facebook (2004) and Twitter (2006) grew and aggregated audiences in their feeds, digital marketers trying to stand out and win traffic started going multimedia, crafting preview images, infographics, and other visual collateral to go out with every new blog post, case study, or announcement.

This multimediaification of the feed created a need for companies to do some basic graphic design work for each new post—frequent but unsophisticated work that companies didn't want to spend a $30/hour designer on.

The basic feature of being able to throw text on top of images became Canva's "sepia filter"—the feature that, like Instagram's filters, got them product-market fit (5 million users in 2 years) by helping marketers create quick, branded social media graphics using free, browser-based tools.

Other products like Unsplash (2013) followed Canva by giving marketers access to high-quality, free stock photography, while on the other hand, Buffer launched Pablo (2015) to use a free social media graphic builder as lead gen for their post scheduling product.

Since then, Canva has grown to 265M monthly active users, expanding well beyond social media graphics into presentations, docs, videos, posters, billboards, business cards, and more. The company launched Canva Docs to compete with Google Docs and Microsoft Word, while also pushing into video editing, website creation, and data visualization tools.

The company's biggest product evolution came with their entry into AI. They launched Magic Write (powered by GPT-3) for text generation, followed by Magic Design for instant layout generation, and Magic Edit for image manipulation. Later additions included Magic Switch for converting designs between formats, and Magic Media (powered by Runway) for video generation.

Canva's AI capabilities took a major leap forward with the launch of its Creative Operating System—built around the Canva Design Model, a design-aware foundational AI that generates editable, layered designs across formats. The same release shipped Video 2.0, a new Brand system, Canva Forms, Canva Email Design, and Canva Grow—a full-stack marketing platform integrating the MagicBrief acquisition for AI-powered ad intelligence across more than $6B in analyzed ad spend, starting with Meta. Canva also made Affinity free and began tightly integrating it with Canva for cross-workflow creation; Affinity has since passed 5M downloads.

Canva's full-stack AI strategy combines three layers: (1) its own foundation model (Phoenix) through its acquisition of Leonardo AI (for $370M) that "autocompletes in Canva templates", (2) native AI text, image and video generation features in the app layer powered by OpenAI, Phoenix and Runway ML, and (3) an ecosystem of 120+ plugins for specialized capabilities like AI avatars and voiceovers. Canva AI is available in 16 languages across 31 locales, extending its capabilities into non-English markets.

The current product suite, unified under Visual Suite 2.0, spans docs, presentations, websites, whiteboards, videos, and spreadsheets in a single canvas. The same release introduced Canva Code (for building functional mini-apps), Canva Sheets (data and spreadsheet layer), and AI upgrades to Photo Editor. A key piece of this platform strategy is the mini apps and website builder, which uses AI to let users create functional applications and sites and has reached over 10M monthly active users. This reflects a deliberate repositioning: Canva now describes itself as "an AI platform with a bunch of design tools" rather than "a design platform with AI tools"—a shift they frame as becoming "a cursor for design" or a "design agency in your pocket."

Canva Grow has deepened into a comprehensive video marketing suite, incorporating motion graphics and AI-driven video ad creation capabilities—brought in through the acquisitions of Cavalry and MangoAI—adding programmatic animation and performance-oriented video ad tooling directly into the marketing workflow. The MangoAI deal also brought former Netflix VP Nirmal Govind on board as Canva's first Chief Algorithms Officer.

The platform has extended further into agentic AI and marketing automation through the acquisitions of Simtheory and Ortto. Simtheory adds agentic AI workflows, enabling Canva to automate multi-step creative and marketing tasks beyond single-turn generation; Ortto brings a customer data platform and marketing automation layer, extending Canva from content creation into campaign orchestration and audience targeting. These capabilities are productized in Canva's AI Assistant, which can autonomously call tools across the platform to execute end-to-end design workflows—taking a user prompt and completing multi-step tasks like sourcing assets, applying brand settings, and generating layouts without manual intervention.

Canva AI 2.0, launched in research preview and described by the company as the most significant product evolution since its 2013 founding, generates fully layered, editable outputs from natural language prompts and introduces an architecture for conversational design, iterative agentic editing, layered object intelligence, and memory. New workflows include connectors, scheduling, web research, brand intelligence, Sheets AI, and Canva Code 2.0.

Canva's developer platform has expanded with 12 new APIs—including a Design Editing API and Data Connectors—alongside a Premium Apps Program, enabling enterprises like Meta and Ray White to embed Canva's creation layer directly into their own workflows.

Canva is actively integrating with chatbots like ChatGPT and Claude, treating them as top-of-funnel acquisition platforms. Users can now create, preview, and edit Canva designs directly inside ChatGPT (available to Free, Plus, and Pro users outside the EU), and Canva has become one of the top 10 referred domains from ChatGPT, with users logging over 26M conversations with the Canva app on the platform. Canva's MCP integration with Claude launched in July 2025, and a deeper Claude Design integration with Anthropic Labs (announced April 2026) lets Claude-generated drafts and code be imported into Canva as fully editable designs. Traffic through LLM referrals now represents double-digit percentages, and the company is allocating resources to optimize for LLM search results alongside traditional SEO.

Operating profitably for the past 7 years with a highly efficient product-led growth (PLG) sales motion gives Canva the free cash flow to invest heavily into AI and enterprise sales simultaneously without large, repeated capital fundraises.

Competition

Adobe

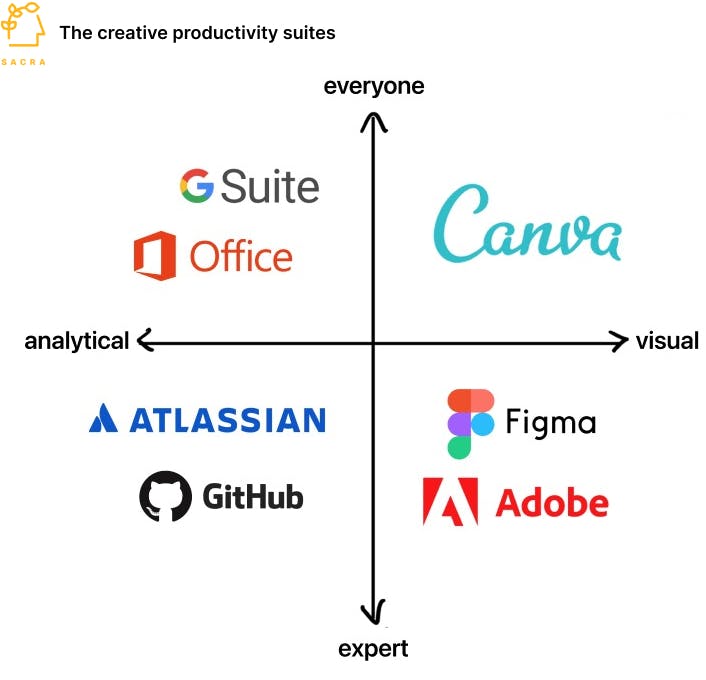

Adobe's Creative Suite, including Photoshop and Illustrator, remains the industry standard for professional designers. While these tools offer more advanced capabilities, they require significant training and are often prohibitively expensive for casual users or small businesses. Canva has positioned itself as a more accessible alternative, focusing on speed and ease of use rather than advanced editing features. This approach has allowed Canva to capture a large segment of the market that was previously underserved by complex professional tools.

In October 2025 at Adobe MAX, Adobe announced Firefly Image Model 5 with layered image editing and native 4MP image generation, rolled out Generate Soundtrack and Generate Speech (15 languages, emotion tags, leveraging ElevenLabs), introduced a browser-based multi‑track Firefly video editor waitlist, and previewed Project Moonlight plus a ChatGPT integration—steps that intensify competition with Canva’s AI-driven design and video tooling.

AI design tools

Microsoft Office and Adobe Creative Cloud—which 100M+ organizations already pay for—which are aggressively investing in generative AI via Bing Image Generator (1 billion images created so far) and Firefly (3 billion images created) to own graphic design and image creation.

The rise of multimodal LLMs like Google’s Gemini and OpenAI’s GPT-Vision that can process both text and images threatens graphic design tools like Canva by drastically undercutting human designers on price (at roughly $0.005 per image) and replacing WYSIWYG editing with natural language prompts.

Where Canva consists of a core editing technology applied to different sizes of rectangles to make everything from business cards to billboards, Gamma and Tome are forging a new interactive, responsive “mini-website” form factor that breaks free from the dimensions of physical paper and fixed screen sizes.

While ChatGPT generates text and Midjourney generates images, Gamma’s AI editor is multimodal, allowing users to generate rich cards with text, images, tables, timelines, 2x2 diagrams, and more.

Figma

Figma is a browser-based online design tool used to build mock-ups, wireframes, product diagrams, and other visual collateral primarily focused around the designer and product manager roles.

Figma's lack of direct substitutes makes it hard for teams to stop using it once they've become accustomed to its workflow. Teams use Figma for brainstorming, prototyping, user research, and to hand off the design system to developers—other tools don't do all of that.

Figma is relatively easy to self-serve into even for bigger companies because IT departments that centralize purchasing on software like Salesforce or Hubspot will devolve buying decisions on tools like Figma to the design team thanks to (1) the lower, more flexible pricing, and (2) the less sensitive files involved.

While both are bucketed as design products, only about 20% of Canva's use cases ultimately overlap with Figma's. Canva differentiates with features like video editing, presentations, and print—and from our research, teams will frequently pay for both tools with Figma being used more on the product side of the organization and Canva being used more on the marketing side.

Web-based design tools

Canva's primary competition in the free, easy-to-use, and web-native category of graphic design tools comes from companies like Visme and Snapseed offer similar drag-and-drop interfaces and template libraries for creating graphics, presentations, and social media content.

However, Canva differentiates itself through its extensive template library (over 500,000 designs) and intuitive user interface that requires minimal learning curve. Canva's Brand Kit feature, which allows users to save brand assets and apply them consistently, is a key advantage for small business users.

Content marketing platforms

TAM Expansion

Canva's expansion and transition from simple graphic design tool to enterprise productivity suite has them on a collision course not just with Adobe's Creative Cloud ($275B market cap), but Microsoft Office ($2.23T), Wix ($10B) and others.

Enterprise

Canva Enterprise, one year after its launch, is now used by 95% of the Fortune 500. Case studies include FedEx rolling Canva out across 1,400 teams in 45 countries and cutting brand review time by 77%, and Docusign saving $300K in design hours while increasing sales engagement by 50%. This penetration rate positions Canva's B2B segment as a credible displacement threat to Microsoft Office and Google Workspace within marketing and creative workflows.

Productivity Suite

Canva is betting big on the primacy of the rectangle, drilling down into different industries like education and different rectangle types—collaborative whiteboards competing with Figma ($400M ARR) and Miro ($17.5B valuation), slides competing with Google Slides (2B+ Workspace users), and one-page websites competing with Squarespace ($931M revenue).

Canva is stitching together this suite of rectangle-designing tools into a full suite of products, leveraging their ownership of companies' brand assets and marketing workflows to own the entire productivity suite.

Their long-term goal is to displace the traditional productivity suite of email, word processor, and spreadsheet with the visual communication tools—slides, images, and videos—that have become essential for every role in an organization, from sales & marketing and product to HR.

International

Canva has been aggressively pursuing international expansion, with a focus on localizing its product for different markets. The company now operates in over 190 countries and supports over 100 languages. Canva has been particularly successful in emerging markets like Brazil, India, Indonesia, and the Philippines, where it often serves as the first design tool many users encounter. This global approach has been key to Canva's rapid user growth and its ability to tap into diverse market opportunities. The company's goal of reaching 1 billion users in the coming years would represent a substantial expansion of its total addressable market.

Video Marketing

Video marketing represents an increasingly distinct TAM within Canva's expansion strategy. Through Canva Grow—extended by the acquisitions of Cavalry (motion graphics) and MangoAI (AI-driven video ad creation)—Canva is pushing into paid video advertising workflows that have historically been served by dedicated creative automation platforms. For performance marketers, this positions Canva not just as a content creation tool but as an end-to-end creative production layer for paid campaigns.

Marketing Automation

The acquisition of Ortto—a customer data platform and marketing automation tool serving 11,000 customers across 190 countries—opens a new TAM beyond content creation: the broader marketing technology stack covering audience segmentation, campaign orchestration, and lifecycle messaging. This puts Canva into direct competition with HubSpot and Mailchimp for SMB marketing workflows, with a distribution advantage of 265M existing users.

Developer Platform

Canva's developer platform—built around 12 new APIs including a Design Editing API and Data Connectors, plus a Premium Apps Program—has opened a developer and enterprise integration TAM. Enterprises like Meta are already embedding Canva's creation layer into their own tools, creating a potential platform revenue stream and stickiness flywheel that mirrors the paths taken by Salesforce and Figma's plugin ecosystems.

Canva's long-term upside hinges on how well it can sell this platform into the enterprise with Microsoft Office ($35B ARR) and GSuite (3B+ users) standing in the way.

News

DISCLAIMERS

This report is for information purposes only and is not to be used or considered as an offer or the solicitation of an offer to sell or to buy or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting or tax advice or a representation that any investment or strategy is suitable or appropriate to your individual circumstances or otherwise constitutes a personal trade recommendation to you.

This research report has been prepared solely by Sacra and should not be considered a product of any person or entity that makes such report available, if any.

Information and opinions presented in the sections of the report were obtained or derived from sources Sacra believes are reliable, but Sacra makes no representation as to their accuracy or completeness. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a determination at its original date of publication by Sacra and are subject to change without notice.

Sacra accepts no liability for loss arising from the use of the material presented in this report, except that this exclusion of liability does not apply to the extent that liability arises under specific statutes or regulations applicable to Sacra. Sacra may have issued, and may in the future issue, other reports that are inconsistent with, and reach different conclusions from, the information presented in this report. Those reports reflect different assumptions, views and analytical methods of the analysts who prepared them and Sacra is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report.

All rights reserved. All material presented in this report, unless specifically indicated otherwise is under copyright to Sacra. Sacra reserves any and all intellectual property rights in the report. All trademarks, service marks and logos used in this report are trademarks or service marks or registered trademarks or service marks of Sacra. Any modification, copying, displaying, distributing, transmitting, publishing, licensing, creating derivative works from, or selling any report is strictly prohibited. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of Sacra. Any unauthorized duplication, redistribution or disclosure of this report will result in prosecution.